Global Insights

Is herd head expansion going to continue?

Milk supply outpacing demand so it’s best if dairy prices fall.

U.S. headline milk production growth was much stronger than expected in September, up 4% compared to the forecast of +3.2%. The amount of fat and protein in the milk was also up from last year, which put component adjusted production up an exceedingly strong 6.1%. The biggest surprise was a 21,000 cow upward revision to August, which means the number of herds expanded by 42,000 head between July and August followed by an additional 40,000 cows being added between August and September.

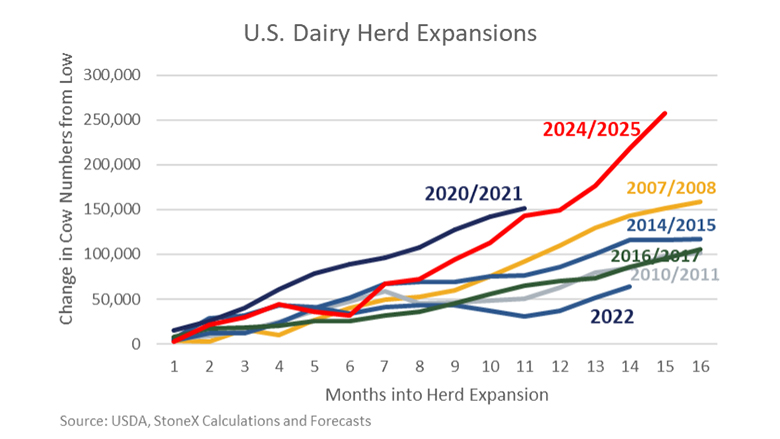

The only other time that we’ve seen an expansion like this was the mid-1980s. The government had paid farmers to stop producing milk for a period of time, and when those payments ran out, the herd (and production) rebounded very quickly. U.S. dairy farmers have now added 258,000 cows (+2.8%) to the herd in 15 months, which is the fastest pace since the mid-1980s. far outpacing any expansion we’ve seen in the past 40 years.

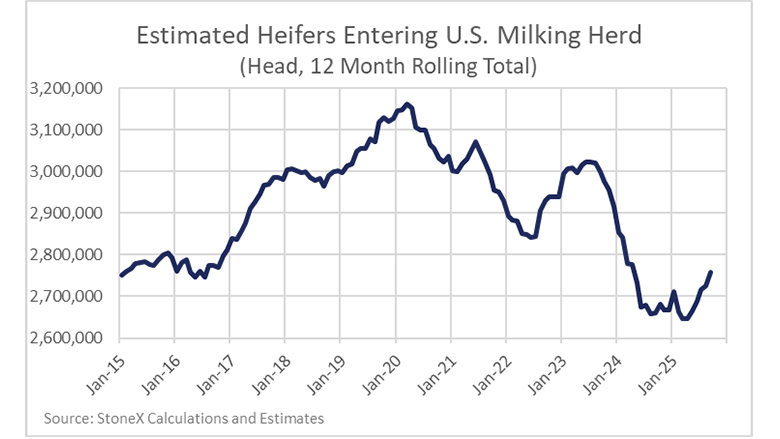

The herd has expanded 258,000 head in 15 months with 186,000 of that coming in the past seven months. With slaughter recently running about flat against last year there is no mathematical way the herd could have increased this much without more heifers coming in. A year ago, there was a lot of talk that there weren’t enough heifers to expand the herd. Yet, dairy farmers undertook the multi-year process of farm expansions and new builds to supply milk into the new processing capacity (mostly cheese) that has been starting up in different parts of the country.

Those farmers adjusted their own breeding programs (or contracted with other farmers) to raise the needed heifers to stock those barns. Of the 258,000 head added to the herd, 222,000 have been in states with significant new processing capacity (Texas, Kansas, New York, South Dakota, Minnesota and Idaho). While the government shutdown has limited some of the needed data for my monthly heifer supply calculations, my best estimate is that in the past seven months about 95,000 more heifers have come into the herd than last year. This means that about half of the recent herd growth is coming from new cows versus holding existing cows longer.

Is this expansion going to continue? The very strong milk production has combined with only modest demand to put milk prices on a year-long downtrend. Calf/slaughter revenue has been helping to keep dairy farm revenue strong, but even cattle prices have come off their record peak a month ago. Farmers who were expanding to capture profitable margins over the past year should start to slow things down in 2026. However, it continues to look like much of the herd/milk expansion has been driven by new processing capacity. If those new plants are running at 100% capacity and all of the milk going into them comes from new farms/cows, then we could still see another 126,000 head added to the herd. I don’t think we are going to add another 126,000 head (we certainly don’t need them), but then again, I didn’t think we would add 258,000 cows in the past 15 months either.

It’s worth talking about data quality. The September Milk Production report was supposed to come out on October 22, 2025, but the Federal government was three weeks into a shutdown, and the USDA was not releasing most of their regular data and reports. As the shutdown stretched into November with no clear end in sight, the USDA announced they would start releasing some reports again which included Milk Production.

Yet, I want to point out that there were only five working days between the public announcement that they would be releasing the September Milk Production report and its actual release. Maybe the USDA was collecting the relevant data during the shutdown? I don’t know, but five days is an extremely compressed timeline to collect the data particularly if data wasn’t collected during October.

Therefore, it’s worth treating this data as preliminary and subject to revision. We won’t have to wait too long for revisions since the October Milk Production report was scheduled to be released on November 21, 2025, less than two weeks after the September report came out.

While the exact numbers for September could be revised, the trend is clear. We’re adding a lot of cows. Milk production per cow is also growing along with the component in the milk. Long-run average growth for component adjusted U.S. dairy demand is 1.9%. Production was up 6.1% in September and we’re on track for 4.2% growth for the full calendar year. Supply is clearly outpacing demand and the job for dairy prices is to fall to a level that boosts demand and starts to slow the supply.

The trading of derivatives such as futures, options, and over-the-counter (OTC) products or “swaps” may not be suitable for all investors. Derivatives trading involves a substantial risk of loss. Past results are not necessarily indicative of future results.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!