State of the Industry 2016: Tea with milk, fruit juice with vegetables are trending

Coffee and milk, tea and milk and fruit juice with vegetables are current trends in the coffee, milk and juice segments.

Detail on porcelain showing the cultivation and harvesting of tea by Jean-Charles Develly. Image courtesy of Gianni Dagli Orti, The Art Archive at Art Resource, New York

Cold-brew is an up-and-coming popular drink in the nondairy beverage space. Austin, Texas-based Chameleon Cold-Brew makes four flavors in 16- and 32-ounce glass bottles and six flavors in 10-ounce bottles.

Tea with milk has become a popular hybrid. Celestial Seasonings, Boulder, Colo., has four latte products, including chai and matcha flavors. Annual sales of ready-todrink protein beverages are about $187 million, according to IRI. A shake from PowerBar has 30 grams of protein.

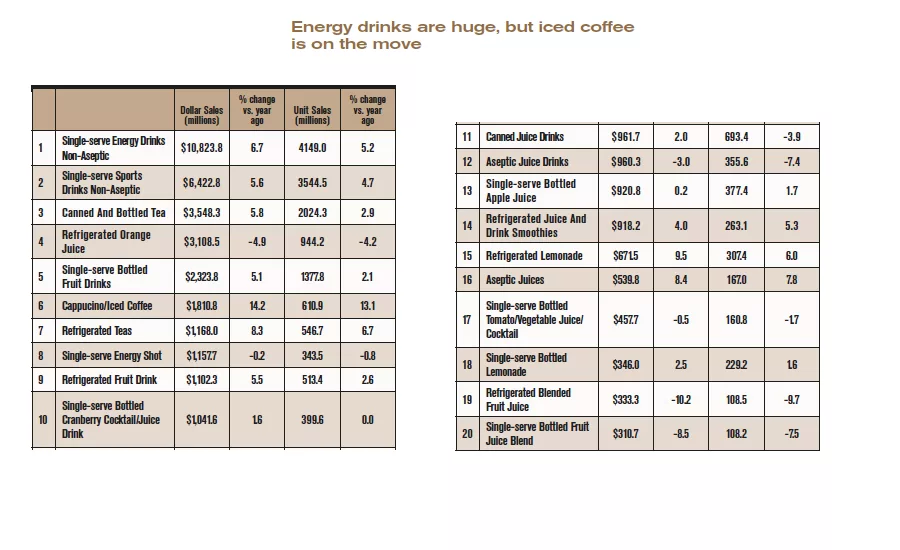

52 weeks ended Sept. 4, 2016. Total U.S. Multi-Outlet w/ C-Store (Supermarkets, Drugstores, Mass Market Retailers, Gas/C-Stores, Military Commissaries and Select Club & Dollar Retail Chains). Source: Information Resources Inc. (IRI), a Chicago-based market research firm. Note: Sales rankings shown are for individual brand line listings, not total brand listings.

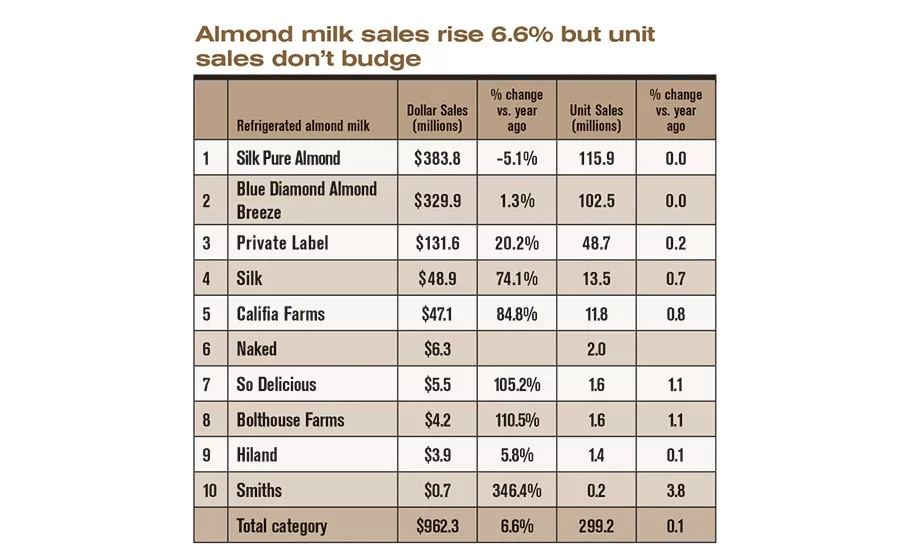

52 weeks ended Sept. 4, 2016. Total U.S. Multi-Outlet w/ C-Store (Supermarkets, Drugstores, Mass Market Retailers, Gas/C-Stores, Military Commissaries and Select Club & Dollar Retail Chains). Source: Information Resources Inc. (IRI), a Chicago-based market research firm. Note: Sales rankings shown are for individual brand line listings, not total brand listings.

Many fluid milk processors manufacture juices, iced tea and coffee beverages. They have the necessary processing equipment and they have relationships with retailers who often want a second brand or control brand to put in their nondairy refrigerated cases. These nondairy beverages represent additional sales opportunities for a dairy.

Milk | Cheese | Cultured | Ice Cream | Butter | Non-dairy Beverages | Ingredients | Exports

Americans drink just as much coffee now as they were in 1999 (about 2.7 cups a day), according to a 2015 Gallup study. Still, the market continues to grow. According to Information Resources Inc., Chicago, dollar sales for the ready-to-drink cappuccino/iced coffee category rose 14% to $1.8 billion and unit sales were up 13% in the 52 weeks ended Sept. 4 in U.S. supermarkets, drug stores, mass merchandisers, gas and convenience stores, military commissaries, and select club and dollar retail chains.

One trend grabbing attention is cold-brew coffee, though experts throw cold water on it. They say the cold-brew segment has not yet grown large enough to significantly impact sales or further penetration.

“Cold brew, despite receiving a lot of attention in the press, remains very niche,” said Eric Penicka, research analyst for Chicago-based Euromonitor International. “On-trade (foodservice) has been the backbone of this, and, until recently, was reserved to independent, specialty coffee shops.”

Yet dairy processors have taken note. This year, national brand Shamrock Farms came out with a ready-to-drink version in 12-ounce bottles. In the Pacific Northwest, Kent, Wash.-based Smith Brothers Farms partnered with Tony’s Coffee on a co-branded cold-brew coffee-and-milk drink in 10-ounce and quart packages. And the trend is not limited to beverages. Tillamook County Creamery Association developed a cold-brew flavored ice cream.

Austin, Texas-based Chameleon Cold-Brew is an up-and-comer. The company’s black cold-brew coffee concentrate is the No. 1 brand by sales, according to IRI. Chameleon Cold-Brew makes four flavors in 16- and 32-ounce glass bottles and six flavors in 10-ounce bottles. The company offers one flavor in 32-ounce bottles exclusively to Target stores nationwide and another for H-E-B and Central Market stores in Texas.

“Ready-to-drink coffees boomed into the market in the past year or two, but still are a sub-segment of a niche category in the market,” explained Lauren Masotti, client manager for U.S. beverages at New York-based Kantar Worldpanel US. “Penetration has stabilized, but frequency has grown — the category attracted users and they really like drinking it.”

Reading the RTD tea leaves

The tea market has evolved over the years as consumers’ on-the-go lifestyles put an emphasis on convenience and ready-to-drink teas. However, natural and organic trends seem to be the next big push within the tea market.

“Natural and organic are very important to tea consumers. However, all-natural is significantly more preferred than organic is,” said Elizabeth Sisel, beverage analyst at Mintel, Chicago. “GMO-free and fair trade claims are also gaining traction, but do not have the same impact on consumer purchasing decisions as does all-natural.”

Varietal trends are impacting the U.S. tea market. According to the Tea Association of the U.S.A., about 85% of American consumers drank black tea and 14% chose green tea in 2015. Oolong, white and dark made up the remaining amounts.

The market is impacted by the trend in hybrid beverage.

“Tea lattes (tea and milk) have continued to be a trend, while sparkling tea is on the forefront of the hybrid market,” Masotti said. “There are some players offering coffee and tea blends — giving consumers the health benefits of tea and the energy boost most often sought [from] the coffee segment.”

Penicka at Euromonitor International also notes that natural is having a greater impact than organic when it comes to hot tea because of its inherent natural properties. RTD tea also is seeing a greater influence when it comes to natural attribute claims.

“Within RTD teas, there has been a very clear movement toward the creation of naturally brewed teas. This continues to bring consumers into the category,” he said.

Sweetener trends, which have posed some challenges for other categories, have had a minimal impact on the RTD tea category because of the vast number of options from which consumers can choose.

“Sweeteners haven’t had the detrimental impact on tea as we’ve seen in other categories,” Penicka noted. “Even where RTD teas are highly sweetened, be it with sugar or artificial sweeteners, consumers are often offered an unsweetened variant. When compared to a category like carbonates, this is a very positive attribute.”

“Sweetened is definitely preferred over unsweetened, particularly lightly sweetened or just sweetened, not necessarily extra sweet,” said Mintel’s Sisel. “Lightly sweetened varieties likely help products keep that health-halo [that] tea already possesses, while perhaps improving the taste for many drinkers.”

She said the majority of consumers want RTD teas to be healthy, but nearly as many also want the drink to be hydrating. “RTD tea’s hydrating and thirst-quenching qualities really help to position it as a drink that can be consumed at multiple drinking occasions,” she said.

Expect consumers to ask for more sophisticated teas and flavors because of what they are seeing in restaurants and tea shops.

“Fueled by premium tea retailers, growing interest in teas [that are] more complex than standard black or green teas has already begun to permeate its way through traditional retail channels like supermarkets with oolong and rooibos teas making their way onto shelves,” Penicka said. “We expect to see more of this development in specialty teas and herbal teas over the forecast period.”

Kantar’s Massoti noted that seasonal varieties are growing in popularity.

“Seasonal flavors have been interesting to follow as more indulgent flavors like pumpkin spice, caramel vanilla and peppermint mocha have become more available in the category,” she said.

New York-based Beverage Marketing Corp. notes the interest millennial consumers show in tea. In its September 2015 report (“U.S. Ready-to-Drink Tea through 2019”), BMC notes that consumers between 18 and 24 years old are 34% more likely than the average consumer to drink RTD tea. It also found that consumers 65 and older are 25% less likely to drink RTD tea than the average consumer. Women are more likely to drink tea than men.

According to the Tea Association’s Fact Sheet, the South and the Northeast have the greatest concentration of tea drinkers.

As the tea market continues to grow, the category has many opportunities to innovate and to keep consumers interested and fuel trial/consumption rates, Sisel said. One trend she is keeping an eye on is carbonated tea as consumers look to different forms of better-for-you carbonated beverages that are outside of the soft drink category.

“Coffee-inspired versions of teas, like RTD lattes, we will likely see more of,” Sisal said. “There is an interest in adding dairy and nondairy milk to RTD teas, and plenty of room for innovation. Functionality is another area for innovation, with many consumers wanting their tea to offer vitamins and minerals, functional energy, etc. More opportunities with matcha teas are also expected, both in RTD and powdered formats.”

Sugar sours juice sales

Although concerns about sugar content have challenged the juice smoothies market, their association as a healthy beverage option have helped the category mitigate contraction. Flavor innovations, including a growth of vegetable juices, also are favorably trending within the category.

As a whole, the juice and juice drinks category contracted 1.8% in total volume in 2014, with not-from-concentrate 100% juice being the only segment not to experience a volume decline, Penicka noted.

“The core reason the juice industry is in decline is the pervasive consumer aversion to sugars and artificial ingredients,” he said. “… Drinks [that] are not 100% juice, as these are more likely to have added sugar, [are] pushing away parents who may have once perceived the products as favorable to carbonates.”

While the percentage of consumers who drink juice and juice drinks has been declining, juice smoothie consumers have nearly doubled since 2010, Kantar’s Masotti noted. “A consumer is 42% more likely to agree with the attitude of ‘to make a healthier choice’ when choosing a juice smoothie as opposed to fruit juice,” she said.

“Green juices with green vegetables have become increasingly common, using items such as spinach, kale, parsley, romaine, cucumber and celery, often combined with a fruit to sweeten the taste,” notes Los Angeles-based IBIS World in an April 2015 report titled “Juice Production in the U.S.”

Euromonitor’s Penicka added that less traditional juice segments, such as coconut, smoothies, pomegranate, etc., have benefited from consumers expanding their juice horizons.

High-pressure pasteurized and cold-pressure processing also gained traction within the juice and juice drink segment as more products using these forms of processing have emerged in the market, analysts note.

“HPP juices are almost exclusively 100% not-from-concentrate juices, and therefore are not laden with added sugars or artificial ingredients, providing consumers with a preferred, premium product,” Penicka said.

The content in this article originally appeared in Beverage Industry, a publication of the Food Beverage Packaging group of BNP Media, publisher of Dairy Foods. The content was condensed and edited by Dairy Foods.

Milk | Cheese | Cultured | Ice Cream | Butter | Non-dairy Beverages | Ingredients | Exports

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!