Rabobank: Global milk production growth to rebalance with retail, foodservice and export dairy demand

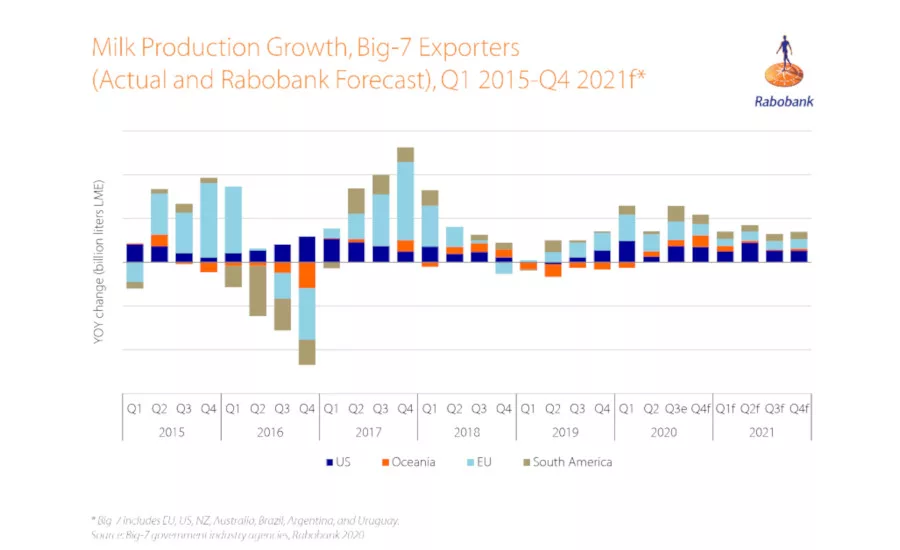

Milk production growth across the major export engines began in quarter two 2020 and is forecast to continue expanding into 2021.

With milk production forecast to grow over the next 12 months and consumption taking time to recover, global market fundamentals are expected to remain weak into quarter two 2021, according to “A Delicate Rebalancing,” a quarter-three 2020 Global Dairy Quarterly report from Rabobank. At that point, the level of exportable surplus should retreat, as domestic consumption improves, the Utrecht, Netherlands-based cooperative bank said.

Milk production growth across the major export engines began in quarter two 2020 and is forecast to continue expanding into 2021, Rabobank said, a feat not matched since 2018. Rabobank expects a 1.3% year-over-year increase in production across the big seven dairy regions in quarter four 2020, 1.0% in the first half of 2021, and 0.8% in the second half of 2021.

Despite the disruptions Covid-19 brought to global dairy markets, farmgate milk prices have been resilient.

“Commodity prices rallied in quarter two, largely on the back of government support in the form of government purchases, inventory management and fiscal stimulus for consumers,” said Sandy Chen, senior analyst – dairy at Rabobank. “However, the outlook for government support is less certain in quarter four and into 2021, which elevates the risk of downward price pressure.”

Rabobank said it observed sequential improvements in foodservice, as more regions have come out of lockdown, while retail dairy sales show early signs of deceleration.

“It will take time for foodservice demand to return to pre-Covid-19 levels, even for countries that have been well ahead of the curve,” Chen said.

Chinese import behavior over the next six to nine months presents uncertainties, with ongoing local milk supply growth and a possible shift in stocking strategy. Rabobank said its updated Chinese dairy imports are still forecast to drop in 2020 and 2021, excluding whey. Loose monetary policies and a weak USD exchange rate will present upside risks to dairy commodities prices.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!