Dairy Market Trends

Milk, Tea and Juice

Let's take a look at what that means for each.

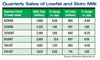

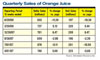

Information Resources Inc., a Chicago-based market research firm, provided data showing that milk sales have been on a bit of roller coaster ride in recent months (see table page 44).

This is from IRI’s scanner based data for its FDMx index (food, drugstores, and mass merchandisers not including Wal-Mart).

For lowfat and skim milk, price spikes led to a 12% increase in dollar sales a year ago. Meanwhile, unit sales have been up one month and down the next. For the most recent available quarter ended June 29, both dollar sales and unit sales dropped significantly. Although not shown here, overall milk sales dropped by nearly the exact same proportions in the same period. For the 52 weeks ended Aug. 10, overall milk sales were up more than 12% by dollar sales, but unit sales dropped about 3.7%.

According to IRI’s FDMx numbers, orange juice sales have also been up and down, but unit and price have ridden the roller coaster together.

In the second quarter of this year, both dollar and unit sales grew about 5%. In the period ended June 29 however, OJ sales dropped more than 10% by both measures, compared to the same period a year before.

Refrigerated tea has been a strong growing category for many years, as consumers warm to tea’s health benefits.

IRI’s numbers have shown strong sales increases at retail for several years running. The most recent, for the 52 weeks ended Aug. 10, show many of the top brands experiencing double-digit dollar sales growth in terms of both dollar sales and unit sales. The pie chart shows the top brands by dollar sales for the period.

Our partners at Mintel Research say the Ready to Drink Category is strong in general and that tea is among its stars.

Ready-to-drink teas have been bolstered by their strong healthy halo. Black, white, red and green teas-already considered to be antioxidant-rich “superfoods”-have strengthened their nutritional profile with the addition of superfruit ingredients. Pomegranate and açaí have been among the most popular.

Juices are bolstered by their natural healthy halo-a benefit that companies have been quick to highlight. In particular, “superfruit”-based juices have gained mainstream traction in recent years. Pomegranate is now a well-established juice flavor, paving the way for other emerging superfruits including açaí and goji berry. But the superfruit landscape is always changing, and new juice introductions are redefining today’s “it” antioxidant-rich flavors. When Frützzo launched its line of organic yumberry juices, it became the first U.S. company to introduce consumers to this Chinese fruit. Also known as yang-mei or bayberry in its native China, this fruit is rich in antioxidants and vitamins. Yumberry is still unknown to most consumers, but its marketing-savvy name and robust nutrition profile suggest it has tremendous potential in the U.S. juice market.

Yumberry isn’t alone in the emerging superfruit world. Mangosteen (a small, dark purple fruit grown primarily in Southeast Asia), acerola (a Latin American cherry-like fruit packed with vitamin C) and noni (an antioxidant-rich tree fruit that is most commonly associated with Tahiti) are all appearing in more fruit-based drinks. Although their health benefits may be unproven, there is no doubt that these superfruits have caché that appeals to health-conscious consumers.

The natural goodness of fruits is at the heart of another emerging juice trend-health by color. Health by color beverages are typically sold in ranges whose variants are each aligned with a specific color and their accompanying health benefits. Red, for instance, is typically associated with vitamin C and lycopene, which is found in tomatoes, red berries, guava and watermelon.

The natural goodness of fruits is at the heart of another emerging juice trend-health by color. Health by color beverages are typically sold in ranges whose variants are each aligned with a specific color and their accompanying health benefits. Red, for instance, is typically associated with vitamin C and lycopene, which is found in tomatoes, red berries, guava and watermelon.

The concept of health by color is well understood in Asia, but this trend has only recently gained momentum in Western markets. Last year in Italy, Parmalat was one of the first European companies to embrace health by color, via its Five Colors of Health line in red, white, green, yellow and blue varieties. U.S. manufacturers have followed suit by offering their own health by color juices. This year Lakewood launched a line of health by color juices under its Fruit Garden brand. Green and Red Fusion, Purple Harmony, Summer Gold and Blue Balance are among the color-centric choices. Naked Juice and Bolthouse Farms also offer color-based smoothies and juices. At a time when healthy options can seem overwhelming, the simplicity of health by color beverages could resonate powerfully with nutrition-conscious consumers.

Beverage Segments in Flux

Milk is the central beverage for dairy processors, but tea and juice play an important role in the business too. All three have been affected by major changes in the consumer attitudes toward all beverages in recent years.Let's take a look at what that means for each.

Milk and milk prices

One of the biggest influences on milk sales in the last two years has been a high price. While it seems the price of everything is higher lately milk had a head start, and to some extent we can see that in the sales numbers.Information Resources Inc., a Chicago-based market research firm, provided data showing that milk sales have been on a bit of roller coaster ride in recent months (see table page 44).

This is from IRI’s scanner based data for its FDMx index (food, drugstores, and mass merchandisers not including Wal-Mart).

For lowfat and skim milk, price spikes led to a 12% increase in dollar sales a year ago. Meanwhile, unit sales have been up one month and down the next. For the most recent available quarter ended June 29, both dollar sales and unit sales dropped significantly. Although not shown here, overall milk sales dropped by nearly the exact same proportions in the same period. For the 52 weeks ended Aug. 10, overall milk sales were up more than 12% by dollar sales, but unit sales dropped about 3.7%.

Juice sales and tea brands

Like milk, juice in some cases has a direct connection to an agricultural commodity that can be affected by supply and demand fluctuations. Orange juice is particularly important for dairy processors, many of whom bottle and sell it. And orange juice in particular is affected by crop fluctuations.According to IRI’s FDMx numbers, orange juice sales have also been up and down, but unit and price have ridden the roller coaster together.

In the second quarter of this year, both dollar and unit sales grew about 5%. In the period ended June 29 however, OJ sales dropped more than 10% by both measures, compared to the same period a year before.

Refrigerated tea has been a strong growing category for many years, as consumers warm to tea’s health benefits.

IRI’s numbers have shown strong sales increases at retail for several years running. The most recent, for the 52 weeks ended Aug. 10, show many of the top brands experiencing double-digit dollar sales growth in terms of both dollar sales and unit sales. The pie chart shows the top brands by dollar sales for the period.

Our partners at Mintel Research say the Ready to Drink Category is strong in general and that tea is among its stars.

Ready-to-drink teas have been bolstered by their strong healthy halo. Black, white, red and green teas-already considered to be antioxidant-rich “superfoods”-have strengthened their nutritional profile with the addition of superfruit ingredients. Pomegranate and açaí have been among the most popular.

Juice trends

Mintel Research also notes that the proliferation of retail beverage choices over the last several years has been good news for U.S. consumers, but the same can’t be said for juice manufacturers. According to Mintel Oxygen Reports, the U.S. fruit juice and juice drink market was valued at $14.7 billion in 2007, but that represents a 4.5% drop from the previous year. To combat that decline and recapture share from competing segments, the U.S. juice industry is focusing on innovation and new consumer needs.Juices are bolstered by their natural healthy halo-a benefit that companies have been quick to highlight. In particular, “superfruit”-based juices have gained mainstream traction in recent years. Pomegranate is now a well-established juice flavor, paving the way for other emerging superfruits including açaí and goji berry. But the superfruit landscape is always changing, and new juice introductions are redefining today’s “it” antioxidant-rich flavors. When Frützzo launched its line of organic yumberry juices, it became the first U.S. company to introduce consumers to this Chinese fruit. Also known as yang-mei or bayberry in its native China, this fruit is rich in antioxidants and vitamins. Yumberry is still unknown to most consumers, but its marketing-savvy name and robust nutrition profile suggest it has tremendous potential in the U.S. juice market.

Yumberry isn’t alone in the emerging superfruit world. Mangosteen (a small, dark purple fruit grown primarily in Southeast Asia), acerola (a Latin American cherry-like fruit packed with vitamin C) and noni (an antioxidant-rich tree fruit that is most commonly associated with Tahiti) are all appearing in more fruit-based drinks. Although their health benefits may be unproven, there is no doubt that these superfruits have caché that appeals to health-conscious consumers.

The concept of health by color is well understood in Asia, but this trend has only recently gained momentum in Western markets. Last year in Italy, Parmalat was one of the first European companies to embrace health by color, via its Five Colors of Health line in red, white, green, yellow and blue varieties. U.S. manufacturers have followed suit by offering their own health by color juices. This year Lakewood launched a line of health by color juices under its Fruit Garden brand. Green and Red Fusion, Purple Harmony, Summer Gold and Blue Balance are among the color-centric choices. Naked Juice and Bolthouse Farms also offer color-based smoothies and juices. At a time when healthy options can seem overwhelming, the simplicity of health by color beverages could resonate powerfully with nutrition-conscious consumers.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!