2019 Dairy 100: Big, Bigger and Biggest

Our 26th annual Dairy 100 ranks the largest companies and cooperatives in the North American dairy industry.

The past year brought challenges to many North American dairy processors, from tariffs threatening export sales to a growing array of dairy alternatives squeezing limited shelf space. Some dairy processors fared better than others when it came to addressing those challenges.

Our latest Dairy 100 rankings, based on 2018 revenues (or the most recent available), reflect those ups and downs, as well as recent expansions, acquisitions, divestures and more.

No changes in the top five

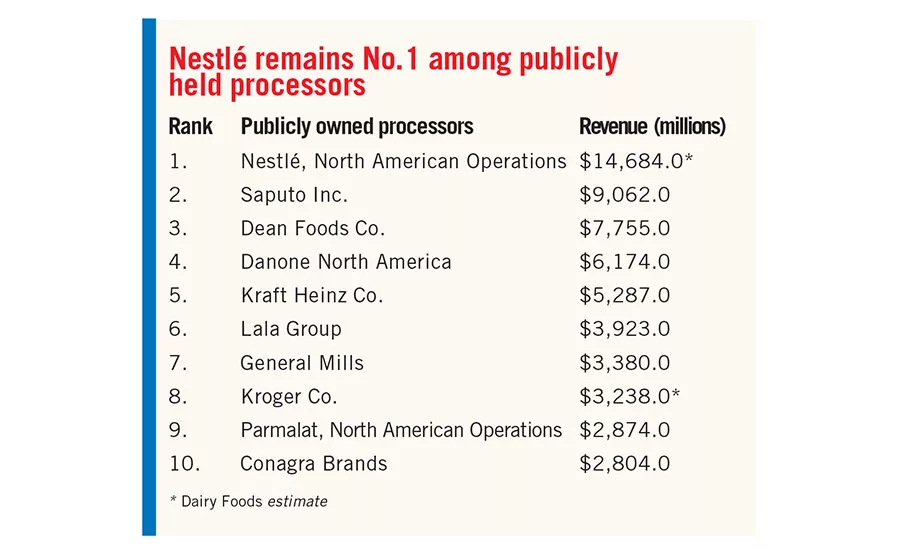

The companies that were among the top five on last year’s list made a return this year, in the same order: Nestlé, North American operations (1), Saputo Inc. (2), Dean Foods Co. (3), Danone North America (4) and Kraft Heinz Co. (5). One of those North American giants, Saputo, made very impressive gains — to the tune of almost $1 billion. However, both Dean Foods and Kraft Heinz lost some ground in 2018.

Rounding out the top 10 are No. 6 Agropur (No. 7 last year), No. 7 Schreiber Foods (No. 6 last year), No. 8 Dairy Farmers of America (DFA, same as last year), No. 9 Lala Group (not in the top 10 last year) and No. 10 Land O’Lakes Inc. (No. 9 last year).

A few newbies

Newcomers to the list this year are Turkey Hill Dairy (No. 72) and Aurora Organic Dairy (No. 86).

Kroger Co. sold Turkey Hill Dairy to a private equity firm back in April. Although our standings are based on 2018 sales data, we list the companies as they exist in the present. So we separated Turkey Hill Dairy’s 2018 revenues from Kroger’s (which also impacted the sales we reported for Kroger).

As for Aurora Organic Dairy, the processor likely should have been on our 2018 list. But we were unable to find a reliable source for estimating the company’s sales at the time.

Notably absent from this year’s list are Hormel Foods Corp. (No. 44 last year), Fieldbrook Foods (No. 80 last year) and F&A Dairy Products (No. 81 last year). We delisted Hormel because the company sold its CytoSport business and thus no longer owns the Muscle Milk and Evolve brands. Wells Enterprises (No. 30) acquired Fieldbrook Foods in April, and Saputo snatched up F&A Dairy Products toward the end of 2018.

Also not appearing on this year’s list is Michael Foods Group (No. 20 on last year’s list). In its place is parent company Post Holdings Inc. (No. 79), which no longer reports on its Michael Foods Group separately. We included the estimated sales for Post Holdings’ Crystal Farms and Crescent Valley dairy brands.

Some of the big gainers on this year’s list, meanwhile, include No. 11 General Mills (No. 38 last year), No. 37 Fairlife (No. 47 last year) and No. 87 Ellsworth Cooperative Creamery (No. 100 last year). Although the latter two companies’ upward movement reflects sales gains, General Mills actually should have been ranked higher on last year’s list (the 2019 rankings include a corrected figure for 2017).

Worth noting

Company acquisitions in 2018 helped boost at least one of the listed dairy processors’ numbers. In addition to acquiring F&A Dairy Products, Saputo purchased Shepherd Gourmet Dairy. The Canadian company manufactures, markets and distributes a variety of specialty cheeses, yogurt and skyr (Icelandic-style yogurt), Saputo said.

Saputo also acquired the activities of Murray Goulburn Co-Operative Co. Ltd. in Australia. According to Saputo, the company produces a full range of dairy foods, including milk, milk powder, cheese, butter and dairy beverages, as well as a range of ingredient and nutritional products such as infant formula. (Saputo made additional acquisitions in 2019.)

Plant closures, meanwhile, were the reality for at least one other dairy processor. Seven fewer plants show up on Dean Foods’ listing in comparison to last year’s version.

The dairy giant has been struggling in the face of declining milk sales and escalating costs. But CEO Ralph Scozzafava was optimistic in his remarks shared in the May 7, 2019, press release announcing Dean Foods’ first-quarter 2019 results.

“The first quarter was a productive period, setting the stage for the sequential improvement in our performance that we expect to achieve throughout 2019,” he said. “Adjusted operating loss is on track with our internal full-year plan and marked an improvement from the fourth quarter of 2018 but was significantly down compared with the year-ago period.

“Our results improved in each month of the first quarter, and we are encouraged by the underlying trends that we are seeing in operations,” he continued. “While we continue to overlap certain customer volume that exited our system last year, we believe we have passed the inflection point as the transformative actions implemented over the past 12 months through our enterprise-wide cost productivity plan are taking hold.”

How we compiled the list

We began our research by contacting all of the company’s on last year’s Dairy 100 list to request information, including their 2018 (or most recent) revenues and any other updates. We also requested information from companies that almost made last year’s list or underwent a growth spurt in 2018.

For public companies that did not respond to us, we relied on publicly available information regarding revenues. For private companies and cooperatives, we estimated revenue — relying, in part, on sources that include but are not limited to market research firm data and reports from Forbes and other publications. It’s worth noting that some dairy companies that likely should be on this list (e.g., Mullins Cheese Inc.) are not because we were unable to locate enough information to formulate an estimate.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!