Are U.S. Exporters Up to the Task?

The world market affects all dairy processors, whether or not they export.

Students, class is in session. To review, please refer back to 2008-09. U.S. dairy exporters capitalized on growing world demand from the middle of the decade to post record export levels, then lost more than one-third of those sales in a matter of months during the global economic crisis. The share of U.S. milk supply sold overseas plunged from nearly 13% to 8%. When that unwelcome product washed back into U.S. shores, the oversupplied domestic market had no home for it except manufacturer and government warehouses, despite its rock bottom price.

Students, class is in session. To review, please refer back to 2008-09. U.S. dairy exporters capitalized on growing world demand from the middle of the decade to post record export levels, then lost more than one-third of those sales in a matter of months during the global economic crisis. The share of U.S. milk supply sold overseas plunged from nearly 13% to 8%. When that unwelcome product washed back into U.S. shores, the oversupplied domestic market had no home for it except manufacturer and government warehouses, despite its rock bottom price.

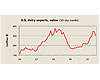

Turn ahead two years, and the global market returned to its longer term trend, leaving the domestic market in better balance. From April to July, U.S. dairy export volumes were up more than 50% from the prior year. By value, shipments were up nearly 80%. The volume of U.S. milk solids shipped offshore was, once again, equivalent to 13% of U.S. production.

Moreover, this business has been lucrative: world dairy commodity prices at the end of the third quarter were 20-60% higher (depending on product) than the year before, and 60-80% above U.S. support prices.

This export resurgence has enabled the next phase of growth in the U.S. dairy industry. Milk production in the June-to-August period was up 2.7%, nearly twice the historical expansion rate. With domestic consumption flat in 2010, the export market is again absorbing our incremental supply.

And that is the crux of today’s assignment - how do we avoid a repeat of the boom-bust cycle seen in 2008-09?

“If the U.S. dairy industry wants to solve the chronic problem of milk (commodity) price variability, it will have to resolve the issue of the variability in the role of export markets as a source of demand for U.S. dairy products,” wrote Brian Gould, associate professor of agricultural and applied economics at the University of Wisconsin-Madison, in fall 2009.

The Bain Globalization Report, developed last year by the Innovation Center for U.S. Dairy, took this concept a step further: “Globalization’s impact is pervasive enough to affect all domestic dairy companies throughout the value chain, whether or not they choose to directly participate in international dairy trade,” it states. “A ‘do-nothing’ strategy is both insufficient and dangerous to the health of the sector.”

Softball question: why is the world dairy market so volatile?

“A part of the reason why the rises and falls in dairy commodity markets are so dramatic is that the volume of international dairy trade is a very small percentage of total world milk production,” explains Jon Hauser, editor of Xcheque.com, a web-based newsletter published out of Australia. “International trade is roughly 7% of world production. If global demand or supply moves by 1%, a relatively small number by any standards, the product shortage or surplus equates to 14% of free global trade. It is extremely difficult to buffer this level of variation through stock movements.”

At the onset of the fourth quarter, the world dairy markets are, by most accounts, in balance, despite supply growth around the world. In addition to expansion in the United States, European milk production was up almost 2% this summer, Australian output was up about 4%, New Zealand was around 5% higher and South American countries saw increases approaching double-digits.

Economic growth in net importing countries has been a key driver of dairy trade, says Rabobank International.

“The economic environment is … supportive in developing regions,” the bank says in its September 2010 Dairy Quarterly. “China’s growth looks increasingly robust and is pulling along much of developing Asia with it. Good growth is also being registered in regions like Latin America. Second quarter results for Southeast Asian processors continued to show robust sales growth.”

Aggressive buying by China has underpinned the world market this year, analysts note. China imported 227,000 tons of whole milk powder from January through August, up from just 20,000 tons in the same period two years ago. With New Zealand focusing its plant capacity on serving this huge market, Kiwi supplies of dairy protein or milk fat are off compared with a year ago. That has created an opportunity the United States has been able to fill. In fact, through July, U.S. exports of cheese, whey proteins and lactose were running at a record pace, NDM/SMP exports were up 37% and butterfat exports were more than triple year-ago levels.

Increased purchases from Russia, the world’s largest dairy importer, also have contributed to market tightness. “Russia [has] entered the market with renewed vigor as drought conditions impact local milk production and leave processors short of product,” Rabobank writes in its September 2010 Agribusiness Review. Russian cheese imports were up 31% in the first half of the year, and more aggressive buying was reported for the second half prior to an import ban that left some confusion in the market.

Meanwhile, other major buyers also have boosted purchases of key commodities in 2010. For instance, Japan cheese imports were up 11%, South Korea’s were up 23% and Indonesia SMP imports were up 39%.

While trade of cheese and powders has flourished, supplies of butterfat remain tight across the globe. Primary suppliers have directed their production to other products – New Zealand to WMP, Europe and the United States to cheese – leaving butterfat in short supply. In the first seven months of the year, butterfat production from Europe, the United States and Oceania was down about 7% from prior year, a shortfall of close to 140,000 tons. That’s reduced inventories to precarious levels that aren’t expected to be replenished to normal anytime soon.

However, students who completed this course in 2008-09 learned that commodity markets are cyclical by nature. Today’s firm market will inevitably be tomorrow’s sloppy one.

Rabobank is among those who are watching world milk production growth closely. “With export supply availability expected to remain solid through coming months and the temporary fillip of buyers re-entering the market after a period of strategic absence likely to pass, sellers will be hoping that Russian buying proves enduring and that the global economic recovery stays on track to underpin recent price gains,” the bank noted in September.

The aforementioned Globalization Study, a potential blueprint for the U.S. dairy industry going forward, concluded that the sector is not structurally set up to accommodate a more globalized industry. With policy reform debate taking center stage in the year ahead, this is more than just an academic discussion.

“Over time, [the price support program and federal milk marketing orders] have hindered many of the incremental adaptive changes that would have enhanced global competitiveness,” the Globalization Study states. “The price support program has limited the U.S. dairy industry’s product adaptations and specifications that have become global norms. With the government as a ‘backstop’ customer, producers and processors have less need for commercial capabilities. In this way, the support program has incented the U.S. dairy industry to be a residual supplier of global ingredients at lower values and narrowed the channels where U.S. dairy commodities satisfy primary customer needs.

“Additionally, milk marketing orders have led to increased price volatility, as they have limited the opportunity for the utilization of a well-developed forward/futures market for milk. While these federal programs have benefited the U.S. dairy industry in other ways, their role will need reconsideration if the United States intends to play a more active role in the global dairy market,” it concluded.

These issues are central to the dairy policy debate. Against this backdrop, U.S. exporters will have a chance to prove whether they can be consistent suppliers or not. An early assessment is at hand this fall, when rising domestic cheese and butter prices narrowed the gap between U.S. and “world” prices. Have U.S. suppliers created a sufficient value proposition to keep volumes moving?

Today’s review session is now complete. Let the real-life test begin.

Turn ahead two years, and the global market returned to its longer term trend, leaving the domestic market in better balance. From April to July, U.S. dairy export volumes were up more than 50% from the prior year. By value, shipments were up nearly 80%. The volume of U.S. milk solids shipped offshore was, once again, equivalent to 13% of U.S. production.

Moreover, this business has been lucrative: world dairy commodity prices at the end of the third quarter were 20-60% higher (depending on product) than the year before, and 60-80% above U.S. support prices.

This export resurgence has enabled the next phase of growth in the U.S. dairy industry. Milk production in the June-to-August period was up 2.7%, nearly twice the historical expansion rate. With domestic consumption flat in 2010, the export market is again absorbing our incremental supply.

And that is the crux of today’s assignment - how do we avoid a repeat of the boom-bust cycle seen in 2008-09?

“If the U.S. dairy industry wants to solve the chronic problem of milk (commodity) price variability, it will have to resolve the issue of the variability in the role of export markets as a source of demand for U.S. dairy products,” wrote Brian Gould, associate professor of agricultural and applied economics at the University of Wisconsin-Madison, in fall 2009.

The Bain Globalization Report, developed last year by the Innovation Center for U.S. Dairy, took this concept a step further: “Globalization’s impact is pervasive enough to affect all domestic dairy companies throughout the value chain, whether or not they choose to directly participate in international dairy trade,” it states. “A ‘do-nothing’ strategy is both insufficient and dangerous to the health of the sector.”

Softball question: why is the world dairy market so volatile?

“A part of the reason why the rises and falls in dairy commodity markets are so dramatic is that the volume of international dairy trade is a very small percentage of total world milk production,” explains Jon Hauser, editor of Xcheque.com, a web-based newsletter published out of Australia. “International trade is roughly 7% of world production. If global demand or supply moves by 1%, a relatively small number by any standards, the product shortage or surplus equates to 14% of free global trade. It is extremely difficult to buffer this level of variation through stock movements.”

At the onset of the fourth quarter, the world dairy markets are, by most accounts, in balance, despite supply growth around the world. In addition to expansion in the United States, European milk production was up almost 2% this summer, Australian output was up about 4%, New Zealand was around 5% higher and South American countries saw increases approaching double-digits.

Robust demand

Global dairy demand has been robust enough to absorb what’s coming out of the vats, churns and dryers. In the first seven months of the year, the six major suppliers (New Zealand, EU-27, United States, Australia, Argentina and Brazil) increased overall exports of skim milk powder (SMP) by 12%, cheese by 14%, whey proteins by 9% and lactose by 8%, compared with a year ago. Shipments of whole milk powder (WMP) were up 1%, while exports of butterfat were down 11%.Economic growth in net importing countries has been a key driver of dairy trade, says Rabobank International.

“The economic environment is … supportive in developing regions,” the bank says in its September 2010 Dairy Quarterly. “China’s growth looks increasingly robust and is pulling along much of developing Asia with it. Good growth is also being registered in regions like Latin America. Second quarter results for Southeast Asian processors continued to show robust sales growth.”

Aggressive buying by China has underpinned the world market this year, analysts note. China imported 227,000 tons of whole milk powder from January through August, up from just 20,000 tons in the same period two years ago. With New Zealand focusing its plant capacity on serving this huge market, Kiwi supplies of dairy protein or milk fat are off compared with a year ago. That has created an opportunity the United States has been able to fill. In fact, through July, U.S. exports of cheese, whey proteins and lactose were running at a record pace, NDM/SMP exports were up 37% and butterfat exports were more than triple year-ago levels.

Increased purchases from Russia, the world’s largest dairy importer, also have contributed to market tightness. “Russia [has] entered the market with renewed vigor as drought conditions impact local milk production and leave processors short of product,” Rabobank writes in its September 2010 Agribusiness Review. Russian cheese imports were up 31% in the first half of the year, and more aggressive buying was reported for the second half prior to an import ban that left some confusion in the market.

Meanwhile, other major buyers also have boosted purchases of key commodities in 2010. For instance, Japan cheese imports were up 11%, South Korea’s were up 23% and Indonesia SMP imports were up 39%.

While trade of cheese and powders has flourished, supplies of butterfat remain tight across the globe. Primary suppliers have directed their production to other products – New Zealand to WMP, Europe and the United States to cheese – leaving butterfat in short supply. In the first seven months of the year, butterfat production from Europe, the United States and Oceania was down about 7% from prior year, a shortfall of close to 140,000 tons. That’s reduced inventories to precarious levels that aren’t expected to be replenished to normal anytime soon.

However, students who completed this course in 2008-09 learned that commodity markets are cyclical by nature. Today’s firm market will inevitably be tomorrow’s sloppy one.

Rabobank is among those who are watching world milk production growth closely. “With export supply availability expected to remain solid through coming months and the temporary fillip of buyers re-entering the market after a period of strategic absence likely to pass, sellers will be hoping that Russian buying proves enduring and that the global economic recovery stays on track to underpin recent price gains,” the bank noted in September.

Are U.S. exporters ready?

Which brings us to today’s exam. What will U.S. dairy exporters do when market conditions become less favorable? Are they ready to be consistent suppliers, or are they still first-out-last-in residual sellers of last resort?The aforementioned Globalization Study, a potential blueprint for the U.S. dairy industry going forward, concluded that the sector is not structurally set up to accommodate a more globalized industry. With policy reform debate taking center stage in the year ahead, this is more than just an academic discussion.

“Over time, [the price support program and federal milk marketing orders] have hindered many of the incremental adaptive changes that would have enhanced global competitiveness,” the Globalization Study states. “The price support program has limited the U.S. dairy industry’s product adaptations and specifications that have become global norms. With the government as a ‘backstop’ customer, producers and processors have less need for commercial capabilities. In this way, the support program has incented the U.S. dairy industry to be a residual supplier of global ingredients at lower values and narrowed the channels where U.S. dairy commodities satisfy primary customer needs.

“Additionally, milk marketing orders have led to increased price volatility, as they have limited the opportunity for the utilization of a well-developed forward/futures market for milk. While these federal programs have benefited the U.S. dairy industry in other ways, their role will need reconsideration if the United States intends to play a more active role in the global dairy market,” it concluded.

These issues are central to the dairy policy debate. Against this backdrop, U.S. exporters will have a chance to prove whether they can be consistent suppliers or not. An early assessment is at hand this fall, when rising domestic cheese and butter prices narrowed the gap between U.S. and “world” prices. Have U.S. suppliers created a sufficient value proposition to keep volumes moving?

Today’s review session is now complete. Let the real-life test begin.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!