2018 State of the Industry report: Dairy exports are stepping on the gas

On a global scale, the track looks ready for dairy-export growth in 2019

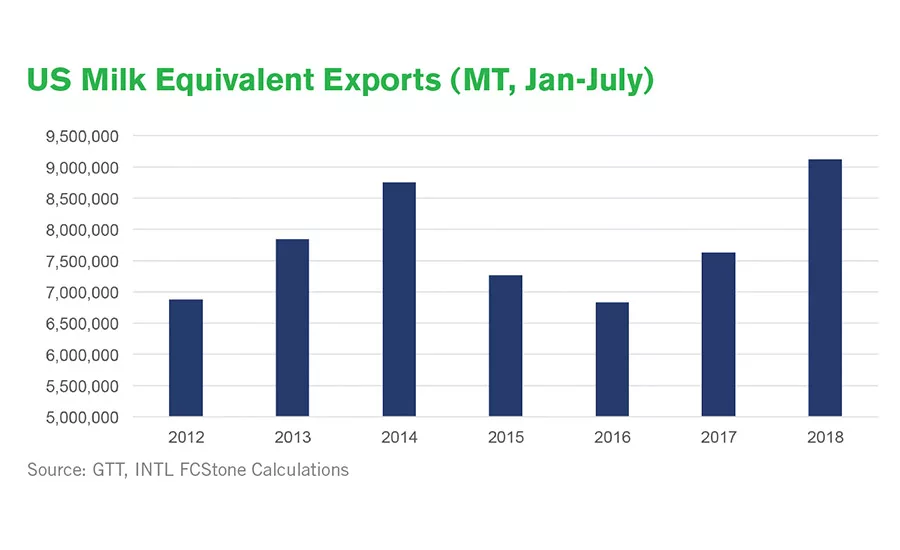

Exports are a demand-pull phenomenon, and demand has been good. U.S. milk equivalent exports from January to July were record high, up 19.5% from 2017.

But it’s not just demand for U.S. products that has been strong; exports were near record high out of New Zealand and the European Union-28 (EU-28) during the first half of the year as well. Overall, the forecast is still for good global demand and growing global imports in 2019, but the United States will be facing some headwinds early in 2019.

Milk | Cheese | Cultured | Ice Cream | Butter | Non-dairy Beverages | Ingredients | Exports

Caution flag flying

Obviously, the retaliatory tariffs that U.S. cheese exports to Mexico and basically all the U.S. dairy exports to China are currently facing is a headwind, but the actual impact might be less than many assume. We don’t have enough hard data to say exactly how the trade flows are adjusting to the increased tariffs yet.

On a milk-equivalent basis, the retaliatory tariffs are now being applied to about 22.6% of U.S. exports. When we work through the likely adjustments in trade flows, we expect to see tariff-affected exports down about 30% from what they otherwise would have been. That works out to a 6.8% reduction in total U.S. exports if the United States can’t find another buyer outside of China or Mexico.

To fully absorb those milk solids, we would need to see exports to destinations other than China and Mexico increase by 8.8% from the level they otherwise would have been. That’s significant, but not unsurmountable.

The bigger issue for U.S. exports will be overall global demand levels and the availability of supply in the other major exporting countries. Let’s start with the easy one, supply.

In Europe, weak farm-gate margins during the first half of 2018 and hot and dry weather over the summer are slowing their milk production growth during the second half of the year. But farm-gate milk prices are rising, and the second half of 2018 looks profitable despite the higher feed costs. That will accelerate EU-28 milk-production growth, with the current forecast for 2019 sitting at 1.7%, up from about 0.8% growth in calendar 2018.

Milk production in New Zealand is primarily pasture-based, so weather will have the final say. But the estimated cost of production in New Zealand is a little under $6.00 New Zealand dollars per kilogram of milk solids, and Fonterra is currently forecasting a payout this season of $6.75.

Fonterra’s forecasted payout is a bit optimistic, with the futures currently suggesting something closer to $6.25. Either way, the New Zealand farmer looks like he will do OK this season, which suggests mild expansion next year. If the weather cooperates, we expect to see New Zealand milk production up about 2.4% for calendar year 2019.

Hitting the apex

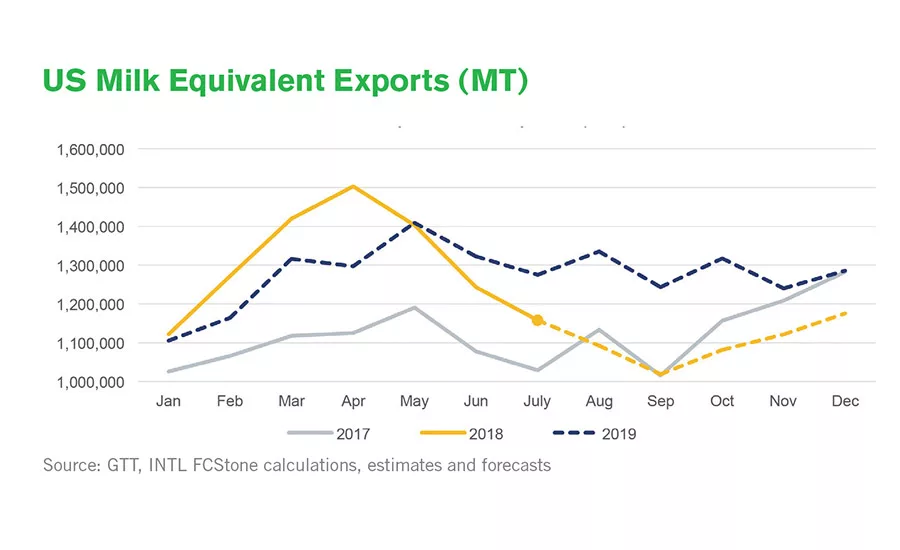

So the United States will likely be facing increased competition in the world market during 2019, plus we will be lapping over a record pace during the first half of 2018. It wouldn’t be surprising to see U.S. exports running a little below year-ago levels during the first half of 2019. But if global demand is as good as expected, we should see exports improve the second half of the year and grow roughly 4% for calendar year 2019.

The outlook for global demand in 2019 is good, but there are downside risks. We track imports into more than 250 destinations and model import demand for the top 31 countries that make up about 85% of global imports, then roll the other 220-plus destinations into a “Rest-Of-World” group and model them together. The models are driven by population, real gross domestic product (GDP) growth, dairy prices and other country-specific variables such as oil prices for large oil-exporting countries.

Out of the top 31 dairy importers, the International Monetary Fund (IMF) is forecasting positive real economic growth in 2019 for 30. In our demand models, if we hold everything else constant, a 1% change in real GDP growth across the major importers results in a 0.8% increase in the quantity of dairy products demanded. So economic growth has a very large impact on dairy demand, and the positive outlook for GDP growth is supportive for dairy demand.

The IMF will be updating its GDP forecasts in October (after this issue goes to press). Given the trade war and worsening economic prospects in a number of developing countries, it’s possible the IMF will revise down their GDP forecasts, which would hurt the outlook for dairy demand in 2019. But we’re likely talking about just minor adjustments to the demand forecast; it doesn’t look like we’re on the edge of a global recession.

On a global scale, the prospects for increasing dairy exports look good for 2019. Positive economic growth is expected for nearly all of the major dairy importers. Oil prices are pushing to the highest levels in years. Dairy prices are generally moderate or low compared to their 10-year ranges.

We should see global imports up about 4%. But the United States will be facing strong competition from the other major exporters, which should keep prices from rising much unless there is a supply problem somewhere in the world or demand turns out much better than expected.

Milk | Cheese | Cultured | Ice Cream | Butter | Non-dairy Beverages | Ingredients | Exports

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!