We may reached the peak of the butter market

The rapid rise in butter prices was driven by lower available supply due to both strong demand and weak milk supplies in key butter-producing regions.

We’re in a time when consumers will eat more butter than at any other time of the year. Most of it will be consumed as cookies, cakes, pies and other baked goods as we celebrate the holiday season. While butter sellers have had the leverage this year, we currently find ourselves in a tenuous time for all companies involved in the global butter market.

CME Butter, after rallying for five straight weeks and hitting an all-time high of $3.5025 per pound on Oct. 6, finally began to show weakness last week. It closed at $3.3975 on Thursday, Oct. 19. Reports indicate demand for butter is slowing, and cream multiples are peaking.

The rapid rise in butter prices was driven by lower available supply due to both strong demand and weak milk supplies in key butter-producing regions. California milk production was down 3.7% in August compared to a year prior, which was slightly better than the July 2023 number, which came in down 5.5% vs the year prior. This was key, considering August U.S. butter production was 2.1% below August 2022 and 12.1% below July 2023.

According to the latest USDA Cold Storage report, butter stocks at the end of August were down 12% from the previous month, yet 4% higher vs. a year ago. According to analysts, the increased consumption may not actually reflect a higher use of butter per capita but rather the changes in buying patterns by restaurants and supermarkets needing to restock refrigerators.

According to the most recent USDA AMS reporting, “Overall, cream is tight in the West, but spot loads are available. Cream volumes above fulfilling contractual obligations gained some looseness in a few parts of the region recently. That said, some butter producers are limiting additional purchases of cream loads due to current prices. Some manufacturers are focusing production lines on keeping retail at full capacity, with cream volumes on the short end to hold both retail and bulk production at full capacity, making bulk butter availability tighter.”

While near-term butter demand appears steady, there is concern that orders will slow down as holiday pipelines near capacity. Buyers are comfortable with hand-to-mouth purchasing but hesitant to take a longer-dated inventory position with prices around near-historical highs.

The market needs to incentivize production, yet butter manufacturers are worried about building expensive inventory with no ability to hedge future sales due to the backwardated butter futures forward curve.

Prices will likely fall further as more cream flows seasonally to the bulk churns. Given the recent demand trends and the volatility of butter prices, multiple credible market analysts anticipate volatility will remain elevated through year-end.

According to the October USDA WASDE report, “Higher-than-expected butter imports in 2024 contribute to a higher fat-basis import forecast. Recent strength in butter prices and expectations of continued firm demand support an increase in the butter price for 2023. For 2024, price forecasts for butter were raised to $2.655 per lb. as price strength is expected to carry into the new year.”

Even for the most bearish buyer, knowing you have your specific butter priced at the market gives you great clarity and lessens the basis risk volatility versus attempting to time the market. Taking advantage of the depressed current forward curve might provide a great opportunity to run fixed-priced or allocation tenders for next year, hopefully at lower prices. Or if you successfully run allocation tenders based on the NDPSR or CME indexes, you always have the ability to fix your upside price risk with CME or OTC-based Butter derivatives.

The opinions expressed in this article are those of the author only and may not represent views expressed by Dairy Foods or its parent company, BNP Media.

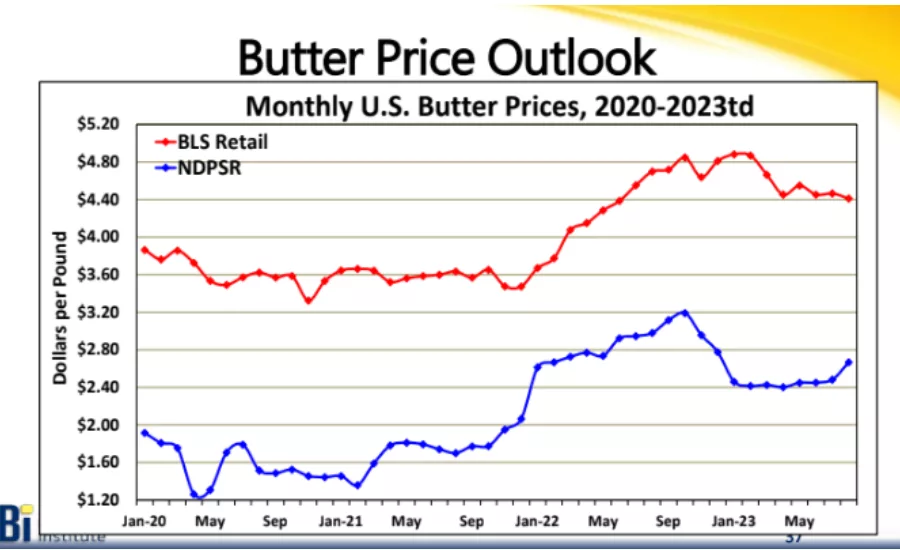

Graphic courtesy of Nui Markets.

Ronald Kevin O'Brien II serves as the President at Nui Markets North America. He is integral to the growth of both the Enterprise and Marketplace digital sales and procurement platforms with his keen understanding of what steps are necessary to integrate Nui into the daily operations of Dairy market participants.

Before joining Nui, Ron spent nine years at Interfood, where he held the position of Global Derivatives Director & Vice President of Interfood Inc. During his tenure, he successfully developed and implemented risk management strategies, analytics, and derivative solutions. Ron played a key role in trade origination and execution, developing the value proposition for derivatives, overseeing and advising Interfood Americas' position management, and providing advisory services to the Interfood Global position committee.

In addition to his professional achievements, Ron holds a finance degree from the University of Florida. He also has a distinguished military background, having served as a sergeant in the United States Marines infantry, with a deployment to Operation Iraqi Freedom in 2003.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!