Dairy Market Trends

Refrigerated iced tea sales continue on a tear, while juice and juice drinks have declined, particularly when measured by unit sales. Meanwhile, sales of both butter and margarine spreads have both been slipping, but looking at margarine and blended spreads in particular it appears that consumers are looking for something they can feel good about.

Refrigerated iced tea sales continue on a tear, while juice and juice drinks have declined, particularly when measured by unit sales. Meanwhile, sales of both butter and margarine spreads have both been slipping, but looking at margarine and blended spreads in particular it appears that consumers are looking for something they can feel good about.

These trends are reflected in data provided by Information Resources Inc. from its scanner-based systems in food, drug and mass merchandisers, excluding Wal-Mart.

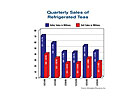

Looking at the quarterly sales figures for refrigerated iced teas, the numbers are good-very good.

During both of the last two quarters, dollar sales were up by more than 30% and unit sales by more than 20%. In fact, the category has seen double-digit growth in each of the last six quarters. Once again, we remind dairy processors that making fresh, refrigerated iced tea is a nice complement to milk, and it’s a great growth opportunity.

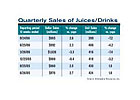

Refrigerated juice and juice drinks, on the other hand have been headed in the other direction, at least by IRI’s accounting. There has been some growth in dollar sales in the last two quarters, but unit sales have been slumping for a year. There may be some extraordinary factors at work here. Orange juice makes up about 2/3 of the refrigerated juice market and orange juice supplies have been impacted by several bad crops. Prices have most likely ridden higher with the short supply.

Refrigerated juice and juice drinks, on the other hand have been headed in the other direction, at least by IRI’s accounting. There has been some growth in dollar sales in the last two quarters, but unit sales have been slumping for a year. There may be some extraordinary factors at work here. Orange juice makes up about 2/3 of the refrigerated juice market and orange juice supplies have been impacted by several bad crops. Prices have most likely ridden higher with the short supply.

Orange juice sales have tracked similarly to overall refrigerated juice, with unit sales sliding for more than a year. But dollar sales are also down a bit for orange juice in recent quarters.

Shifting to another dairy segment, butter and margarine, IRI indicates sales declines as well. The butter category has been up and down from quarter to quarter since early 2005, but there have been more downs than ups. Looking at the top-10 brands of butter, which are not illustrated in the accompanying tables, there has been a good deal of upward movement by some of the top brands, including Horizon Organic and Cabot, both of which had increases of more then 15% in dollar sales during the year ended Nov. 5.

Shifting to another dairy segment, butter and margarine, IRI indicates sales declines as well. The butter category has been up and down from quarter to quarter since early 2005, but there have been more downs than ups. Looking at the top-10 brands of butter, which are not illustrated in the accompanying tables, there has been a good deal of upward movement by some of the top brands, including Horizon Organic and Cabot, both of which had increases of more then 15% in dollar sales during the year ended Nov. 5.

Private label still has about 45% of the butter market, although its share was down a half percentage point for the period.

Spreads, which include margarine and butter blends, are much more brand intensive, with private label accounting for just 7.0% of the current market. The illustration at the right demonstrates how the concerns over trans-fatty acids appear to be impacting the market. Several of the top brands (those in the pie chart are among the top 10), are losing share. The category is slipping overall as well, but sales of the Smart Balance products from ConAgra, which contain no trans-fats or hydrogenated oils, are rocketing. Some of the products in the line are also fortified with Omega 3s.

Refrigerated iced tea sales continue on a tear, while juice and juice drinks have declined, particularly when measured by unit sales. Meanwhile, sales of both butter and margarine spreads have both been slipping, but looking at margarine and blended spreads in particular it appears that consumers are looking for something they can feel good about.

These trends are reflected in data provided by Information Resources Inc. from its scanner-based systems in food, drug and mass merchandisers, excluding Wal-Mart.

Looking at the quarterly sales figures for refrigerated iced teas, the numbers are good-very good.

During both of the last two quarters, dollar sales were up by more than 30% and unit sales by more than 20%. In fact, the category has seen double-digit growth in each of the last six quarters. Once again, we remind dairy processors that making fresh, refrigerated iced tea is a nice complement to milk, and it’s a great growth opportunity.

Orange juice sales have tracked similarly to overall refrigerated juice, with unit sales sliding for more than a year. But dollar sales are also down a bit for orange juice in recent quarters.

Private label still has about 45% of the butter market, although its share was down a half percentage point for the period.

Spreads, which include margarine and butter blends, are much more brand intensive, with private label accounting for just 7.0% of the current market. The illustration at the right demonstrates how the concerns over trans-fatty acids appear to be impacting the market. Several of the top brands (those in the pie chart are among the top 10), are losing share. The category is slipping overall as well, but sales of the Smart Balance products from ConAgra, which contain no trans-fats or hydrogenated oils, are rocketing. Some of the products in the line are also fortified with Omega 3s.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!