Dairy Market Trends

Ice Cream Frozen Yogurt and Novelties

Ice cream sales continued to slip according to year-end sales numbers, but bright spots can be found in the areas of private label and low-fat products. It also appears that novelties are beginning to move in the right direction, and frozen yogurt sales continue to grow, driven by major brands.

Ice cream sales continued to slip according to year-end sales numbers, but bright spots can be found in the areas of private label and low-fat products. It also appears that novelties are beginning to move in the right direction, and frozen yogurt sales continue to grow, driven by major brands.

Meanwhile, new product innovation also appears to be slowing a bit for ice cream, according to Mintel. Again, the exception is in places like churned and other low-fat products and organic ice cream.

Information Resources Inc., reports that for the 52 weeks ended Dec. 30, dollar sales were off 1.2% and units were dropped about 3.8% for the broadest category of ice cream and sherbet. Looking at the same category’s quarterly performance (see table), unit sales have retreated in each of the last five quarters. Dollar sales have also shrunk a bit in most of the quarters, but were up a fraction of a percentage point for the 13 weeks ended Dec. 30. These IRI figures are from the company’s scanner-based measurement tools and reflect food, drugstore, and mass merchandiser sales, other than Wal-Mart.

Information Resources Inc., reports that for the 52 weeks ended Dec. 30, dollar sales were off 1.2% and units were dropped about 3.8% for the broadest category of ice cream and sherbet. Looking at the same category’s quarterly performance (see table), unit sales have retreated in each of the last five quarters. Dollar sales have also shrunk a bit in most of the quarters, but were up a fraction of a percentage point for the 13 weeks ended Dec. 30. These IRI figures are from the company’s scanner-based measurement tools and reflect food, drugstore, and mass merchandiser sales, other than Wal-Mart.

With no massive surge in dollar sales, it does not appear as if ice cream makers are doing much in the way of pass through of higher ingredient prices. In our recent ice cream processor survey, some manufacturers mentioned that they are instead going to smaller unit sizes (from 56 oz to 48 oz).

With no massive surge in dollar sales, it does not appear as if ice cream makers are doing much in the way of pass through of higher ingredient prices. In our recent ice cream processor survey, some manufacturers mentioned that they are instead going to smaller unit sizes (from 56 oz to 48 oz).

Private label accounts for about 21% of the market in the ice cream only category, and private label unit sales were just about flat for the 52 weeks ended Dec. 30. Nearly all of the top brands in the category had lower unit sales for the period-although the Dreyer’s Edy’s Slow Churned brand was close to even. Here is how the top brands faired in terms of unit sales:

Private label accounts for about 21% of the market in the ice cream only category, and private label unit sales were just about flat for the 52 weeks ended Dec. 30. Nearly all of the top brands in the category had lower unit sales for the period-although the Dreyer’s Edy’s Slow Churned brand was close to even. Here is how the top brands faired in terms of unit sales:

Private Label (0.11%)

Breyers (9.28)

Dreyers/Edy’s Grand (16.98)

Dreyers/Edy’s Slow Churned (0.43)

Haagen Dazs (5.88)

Blue Bell (3.88)

Ben & Jerry’s +5.02

Turkey Hill +9.4

Wells (1.6)

Looking at the total number of product launches in 2007, there were less overall and less specifically dairy-based rollouts than there had been in 2006. Non-dairy based introductions increased for the same period.

Looking at the total number of product launches in 2007, there were less overall and less specifically dairy-based rollouts than there had been in 2006. Non-dairy based introductions increased for the same period.

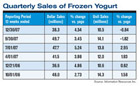

The frozen yogurt category has been reinvigorated of late, and for much of 2007 sales were growing by both dollar and unit measures. The growth seems to have tapered a bit in the last quarter of 2007.

Looking at the top brands of frozen yogurt for the 52 weeks ended 2007, it appears that much of the growth in this category has been driven by the brands of the Dreyers Grand Ice Cream Co., of California. Unit sales of the Dreyers/Edy’s brand grew by 6.2% and it is now the leading brand after private label with more than 17% of the market. The Haagen Dazs brand, also owned by Dreyers, was up 23.5% by unit sales and the combined share of the two brands is 25.4%, which is a bit larger than private label’s share.

Sales of frozen novelties, in general, have also retreated a bit in the last year, but for the quarter ended Dec. 30 dollar sales grew 3.35% and units were up 2.4%, according to IRI. Again, the action is in those products brands that offer the same pleasure with less guilt. Among the fastest growing novelty brands are Weight Watchers (+20% units) and the Skinny Cow (+15%). However, Dove Bars and Haagen Dazs novelties also showed strong growth.

Sales of frozen novelties, in general, have also retreated a bit in the last year, but for the quarter ended Dec. 30 dollar sales grew 3.35% and units were up 2.4%, according to IRI. Again, the action is in those products brands that offer the same pleasure with less guilt. Among the fastest growing novelty brands are Weight Watchers (+20% units) and the Skinny Cow (+15%). However, Dove Bars and Haagen Dazs novelties also showed strong growth.

Looking more closely at product launches for different subcategories, it’s easy to see that product developers are chasing trends. Where overall product development has been trending downward, there were more dairy-based weight control products rolled out in 2006 than in 2007. Also, 26 were introduced in the first five weeks of 2008. The number of churned products debuting in 2007 was lower than in 2006, but 91 products were launched during the two year period and, and seven more at the outset of 2008.

Finally, some numbers to put with the ongoing success stories told of in this month’s Ice Cream Outlook regarding organic ice cream. There were 49 introduced in 2007, as well as 31 in 2006.

Meanwhile, new product innovation also appears to be slowing a bit for ice cream, according to Mintel. Again, the exception is in places like churned and other low-fat products and organic ice cream.

The frozen yogurt category has been reinvigorated of late, and for much of 2007 sales were growing by both dollar and unit measures. The growth seems to have tapered a bit in the last quarter of 2007.

Looking at the top brands of frozen yogurt for the 52 weeks ended 2007, it appears that much of the growth in this category has been driven by the brands of the Dreyers Grand Ice Cream Co., of California. Unit sales of the Dreyers/Edy’s brand grew by 6.2% and it is now the leading brand after private label with more than 17% of the market. The Haagen Dazs brand, also owned by Dreyers, was up 23.5% by unit sales and the combined share of the two brands is 25.4%, which is a bit larger than private label’s share.

Looking more closely at product launches for different subcategories, it’s easy to see that product developers are chasing trends. Where overall product development has been trending downward, there were more dairy-based weight control products rolled out in 2006 than in 2007. Also, 26 were introduced in the first five weeks of 2008. The number of churned products debuting in 2007 was lower than in 2006, but 91 products were launched during the two year period and, and seven more at the outset of 2008.

Finally, some numbers to put with the ongoing success stories told of in this month’s Ice Cream Outlook regarding organic ice cream. There were 49 introduced in 2007, as well as 31 in 2006.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!