Marketing Insights: Profitable Opportunities

The success of U.S. cheese makers and cheese marketers has been the envy of others in the food business for more than two decades.

The success of U.S. cheese makers and cheese marketers has been the envy of others in the food business for more than two decades.

On further examination, however, some segments of the cheese trade are clearly facing some steep challenges. On the other hand, the specialty cheese segment is enjoying unprecedented growth. More importantly, it is profitable growth as specialty cheese makers break free of some of the inherent problems facing commodity cheeses.

Commodity cheeses are an important part of the business, but there is more to the story. First, a look at the commodity side of the ledger.

Commodity cheeses are an important part of the business, but there is more to the story. First, a look at the commodity side of the ledger.

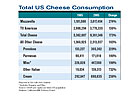

Mozzarella cheese has been the brightest star with consumption growing by 1.9 billion lbs. or 270% during the past 20 years. This is great, but 99% of the mozzarella cheese produced is thin-margin, commodity cheese. It is a market dominated by a few very large producers.

American cheese, the other big boy in the cheese family, experienced growth of just 870 million lbs. or about 130% over the same 20-year stretch. Like mozzarella, much of the production pours out of mega-plants and, for some manufacturers, the margins were and are often slim to none.

Total natural cheese consumption grew by 3.9 billion lbs. or about 185%. So, American cheese consumption growth lagged the total cheese category. A big issue facing American cheese usage has been and continues to be rooted in the processed cheese business. The dilemma is twofold: (1) the composition of processed cheese has changed (less natural cheese is used in many formulations) and (2) processed cheese sales, especially at retail, have been lackluster.

Interestingly, some growth in American cheese consumption can be attributed to specialty cheeses: Excellent growth in aged Cheddar sales and the emergence of numerous flavored (added spices, veggies, etc.) Cheddar, Jack and Colby cheeses have all helped drive American cheese usage.

The U.S. Department of Agriculture only reports consumption data for a few other varieties, but this tip-of-the-iceberg information reveals significant growth in the specialty side of the cheese business.

USDA data, for example, indicate that Parmesan cheese usage increased by 82 million lbs. or nearly twofold between 1985 and 2005. Significantly, virtually all of this growth was home-grown; imports have been flat. It is the same story for Swiss cheese; excellent growth in consumption and limited growth in imports. It is a similar story for Blue cheeses and Romano.

Other growth stories: Provolone cheese consumption grew by 175 million lbs., about 230% between 1985 and 2005. During 2005, cream cheese usage approached 700 million lbs., 2.4 times more than 1985.

That’s about it for consumption data by variety. But USDA also reports an “other miscellaneous” category, which includes a host of varieties. These varieties saw sales nearly double to about one-half billion lbs. by 2005.

The sales volumes of many of these “specialty” cheeses are dwarfed by mozzarella and American cheeses, but the margins per pound are another story. Yes, it costs more to make a specialty cheese, however, the price at the factory typically is not married to USDA’s manufacturing allowances or to the price reported at the Chicago Mercantile Exchange.

Specialty cheese makers add value and extract a more attractive price from the marketplace. For some varieties, demand has clearly outstripped supply, which allows for additional premiums.

Cheese makers in Wisconsin and other Upper Midwest states, and in Vermont and other Northeastern states have seen the light and are well-established purveyors of excellent cheeses. California has recently joined the ranks as a new home to numerous specialty cheese makers. Cheese makers from the Golden State and across the country are capturing awards in international competitions hosted by organizations here and abroad.

A recent study by the California Milk Advisory Board indicates it is a logical home for more specialty cheese production. The state’s supply of lower-cost, high-quality milk continues to grow while supplies contract in some other regions of the country. California is home to a huge domestic market and the state is perched on the Pacific Rim; well positioned for exporting.

More sophisticated consumers and a changing world economic environment will continue to drive, and probably accelerate, growth in the specialty cheese business both here and abroad.

The success of U.S. cheese makers and cheese marketers has been the envy of others in the food business for more than two decades.

On further examination, however, some segments of the cheese trade are clearly facing some steep challenges. On the other hand, the specialty cheese segment is enjoying unprecedented growth. More importantly, it is profitable growth as specialty cheese makers break free of some of the inherent problems facing commodity cheeses.

Mozzarella cheese has been the brightest star with consumption growing by 1.9 billion lbs. or 270% during the past 20 years. This is great, but 99% of the mozzarella cheese produced is thin-margin, commodity cheese. It is a market dominated by a few very large producers.

American cheese, the other big boy in the cheese family, experienced growth of just 870 million lbs. or about 130% over the same 20-year stretch. Like mozzarella, much of the production pours out of mega-plants and, for some manufacturers, the margins were and are often slim to none.

Total natural cheese consumption grew by 3.9 billion lbs. or about 185%. So, American cheese consumption growth lagged the total cheese category. A big issue facing American cheese usage has been and continues to be rooted in the processed cheese business. The dilemma is twofold: (1) the composition of processed cheese has changed (less natural cheese is used in many formulations) and (2) processed cheese sales, especially at retail, have been lackluster.

Interestingly, some growth in American cheese consumption can be attributed to specialty cheeses: Excellent growth in aged Cheddar sales and the emergence of numerous flavored (added spices, veggies, etc.) Cheddar, Jack and Colby cheeses have all helped drive American cheese usage.

The U.S. Department of Agriculture only reports consumption data for a few other varieties, but this tip-of-the-iceberg information reveals significant growth in the specialty side of the cheese business.

USDA data, for example, indicate that Parmesan cheese usage increased by 82 million lbs. or nearly twofold between 1985 and 2005. Significantly, virtually all of this growth was home-grown; imports have been flat. It is the same story for Swiss cheese; excellent growth in consumption and limited growth in imports. It is a similar story for Blue cheeses and Romano.

Other growth stories: Provolone cheese consumption grew by 175 million lbs., about 230% between 1985 and 2005. During 2005, cream cheese usage approached 700 million lbs., 2.4 times more than 1985.

That’s about it for consumption data by variety. But USDA also reports an “other miscellaneous” category, which includes a host of varieties. These varieties saw sales nearly double to about one-half billion lbs. by 2005.

The sales volumes of many of these “specialty” cheeses are dwarfed by mozzarella and American cheeses, but the margins per pound are another story. Yes, it costs more to make a specialty cheese, however, the price at the factory typically is not married to USDA’s manufacturing allowances or to the price reported at the Chicago Mercantile Exchange.

Specialty cheese makers add value and extract a more attractive price from the marketplace. For some varieties, demand has clearly outstripped supply, which allows for additional premiums.

Cheese makers in Wisconsin and other Upper Midwest states, and in Vermont and other Northeastern states have seen the light and are well-established purveyors of excellent cheeses. California has recently joined the ranks as a new home to numerous specialty cheese makers. Cheese makers from the Golden State and across the country are capturing awards in international competitions hosted by organizations here and abroad.

A recent study by the California Milk Advisory Board indicates it is a logical home for more specialty cheese production. The state’s supply of lower-cost, high-quality milk continues to grow while supplies contract in some other regions of the country. California is home to a huge domestic market and the state is perched on the Pacific Rim; well positioned for exporting.

More sophisticated consumers and a changing world economic environment will continue to drive, and probably accelerate, growth in the specialty cheese business both here and abroad.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!