Energy drink segment loses some steam

Lackluster sales of energy shots and aseptic energy drinks slow down the category’s growth.

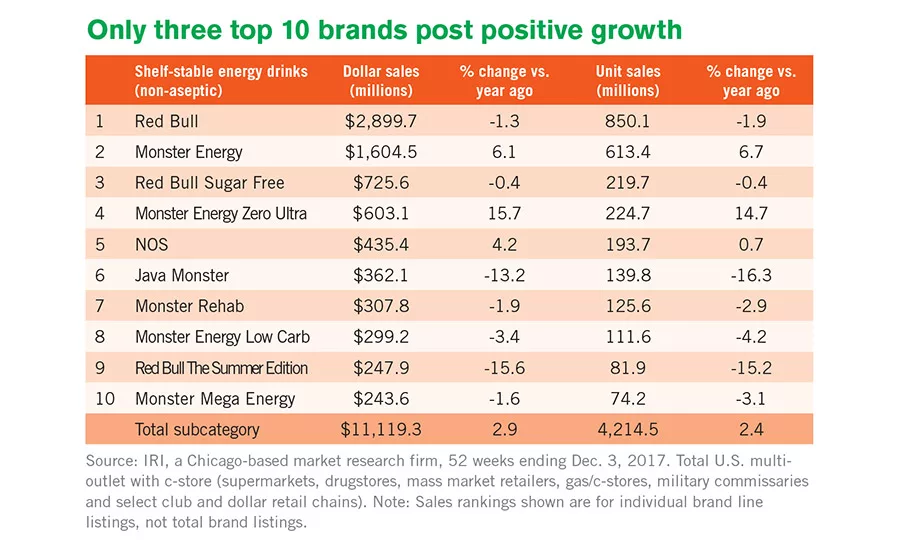

Only three of the top 10 energy drink brands post positive growth

The tired and lethargic among America’s population have been a boon to the U.S. energy drink category.

“The segment has benefited from offering functional benefits with strong appeal to millennials, parents, Hispanics and men 18-34,” said Mimi Bonnet, director, U.S. reports – food, drink and foodservice for global market research firm Mintel, in Mintel’s May 2017 “Energy Drinks — US” report.

But after growing at an annual rate of 7% over the first half of this decade, growth slowed a bit in 2016, according to “Energy & Sports Drinks: U.S. Market Trends & Opportunities,” a May 2017 report from the Packaged Facts division of Rockville, Md.-based MarketResearch.com.

The slowdown continued in 2017 — data from Chicago-based market research firm IRI show only a moderate rate of growth over the 52 weeks ending Dec. 3, 2017. Dollar sales for the total category rose 2.1% to $12.3 billion, while unit sales increased 1.8% to 4.6 billion.

Aseptic options, shots take a dive

Taking part of the blame for the growth slowdown is the aseptic shelf-stable energy drink subcategory. Although the segment is tiny, accounting for less than $85,000 in sales, it realized whopping 81.4% and 76.6% dollar and unit sales declines during IRI’s data timeframe.

Also trending toward the negative was the shelf-stable energy shot subcategory. It realized a 6% dollar sales decline (to $1.1 billion) and a 6.4% unit sales drop (to 318.1 million).

But a number of brands among the top 10 posted strong performance. Dollar sales of private label energy shots jumped 23.1%, while unit sales climbed 34.5%. Tweaker energy shots (Tweaker Energy Drinks), meanwhile, saw a 9.8% increase in dollar sales and a 10.9% rise in unit sales. And Rhino Rush energy shots realized 6.7% and 11.9% dollar and unit sales gains, respectively.

Other brands among the top 10 didn’t fare nearly as well. Rip It Energy Fuel energy shots (Sundance Beverage Co.), for example, realized a 10.5% drop in dollar sales and an 11.2% decline in unit sales. And subcategory leader 5-Hour Energy (Living Essentials LLC) posted 6.2% and 7.9% dollar and unit sales declines, respectively. Stacker 2 Xtra energy shots (NVE Pharmaceuticals) saw similar decreases — 6% and 4.7%.

Sunnier picture for mixes, non-aseptic drinks

Thankfully, the energy drink category’s two remaining subcategories had a good year. Dollar sales within the shelf-stable energy drink mix subcategory rose 14.2% to $88.7 million. Unit sales jumped 14.8% to 35.3 million.

In the larger shelf-stable non-aseptic energy drink segment, dollar sales grew 2.9% to $11.1 billion, while unit sales climbed 2.4% to 4.2 billion.

Leading the top 10 brands in growth were Monster Energy Zero Ultra drinks (Monster Energy Co.), which realized a 15.7% spike in dollar sales and a 14.7% hike in unit sales. “Plain old” Monster Energy drinks also posted strong gains, with dollar sales rising 6.1% and unit sales increasing 6.7%. NOS energy drinks, meanwhile, realized 4.2% and 0.7% dollar and unit sales gains, respectively.

But all seven of the remaining brands in the top 10 lost ground, including subcategory leader Red Bull (Red Bull North America). It saw dollar sales plummet by 1.3% and unit sales drop by 1.9%. A seasonal brand — Red Bull The Summer Edition — lost the most ground among the top 10, with dollar sales falling 15.6% and unit sales decreasing by 15.2%.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!