Ingredients: Pricey Necessities

This past year has been one of the most challenging for dairy foods formulators, as price sensitivity is at an all-time high.

This past year has been one of the most challenging for dairy foods formulators, as price sensitivity is at an all-time high. Innovators are doomed from the get-go, as their base material-milk-costs almost as much as a gallon of gasoline, which of course is a sore spot for distribution economics. Indeed, increasing prices of raw materials, along with the drive for health and wellness are putting pressure on dairy manufacturers to develop innovative, yet cost-effective, value-added products.

This past year has been one of the most challenging for dairy foods formulators, as price sensitivity is at an all-time high. Innovators are doomed from the get-go, as their base material-milk-costs almost as much as a gallon of gasoline, which of course is a sore spot for distribution economics. Indeed, increasing prices of raw materials, along with the drive for health and wellness are putting pressure on dairy manufacturers to develop innovative, yet cost-effective, value-added products.

This is quite challenging when prices for most U.S. agricultural commodities and crop-derived ingredients have exhibited extreme volatility in 2008 and are currently at record levels. For example, in May, Cognis Nutrition & Health, La Grange, Ill., announced its first price increase in more than six years for its natural-source vitamin E and natural plant sterol products. “The rapid escalation in raw material costs plus the steady increase in energy, transportation and packaging costs have reached a point that we can no longer maintain current prices,” said Dave Eckert, vice president North America.

The story was the same for many other ingredient suppliers that provide to the dairy industry. In August, BENEO-Orafti, Morris Plains, N.J., said it would increase the price of its natural, chicory-derived prebiotics by 25%. And in October, FMC BioPolymer, Philadelphia, announced a minimum 15% price increase for all products, as contracts allow. The increase affects microcrystalline cellulose, carrageenan, alginates and propylene glycol alginate product lines.

“FMC BioPolymer continues to dedicate significant resources to identify and implement productivity improvements to mitigate the impact of rising cost,” said Jerry Whelan, global director of sales & marketing. “This price increase will only offset a portion of the increases that our cost-savings programs do not capture.”

“FMC BioPolymer continues to dedicate significant resources to identify and implement productivity improvements to mitigate the impact of rising cost,” said Jerry Whelan, global director of sales & marketing. “This price increase will only offset a portion of the increases that our cost-savings programs do not capture.”

Dominique Speleers, managing director of BENEO-Orafti explained, “BENEO-Orafti has strived to avoid this price increase and has made many improvements within the business to make sure it is running as efficiently as possible. “However, due to the continued and unprecedented increases we have experienced in energy, raw materials and processing costs, a price increase is inevitable and necessary to cover costs and maintain profitability.

“We understand this price increase means extra pressure for our partners and customers. We do know, however, that the consumer recognizes the value and benefits of healthy nutritious foods and is willing and prepared to pay a price premium for such value-added products,” said Speleers.

Indeed, consumers can change their mode of transportation, and even cut back on entertainment and activities, but when it comes to food . . . they must eat. Sure, there are probably fewer steak “date-night” dinners as the home-cooked casserole returns to the family table. But when it comes to dairy foods, the industry has done so much to improve the image of fluid milk and educate consumers about the healthfulness of all dairy foods that we cannot afford to let high prices impact sales.

“Refined sugar prices have been elevated during 2008 since the Savannah Sugar Refinery explosion in February,” says John Curry, president, Sweetener Solutions LLC, Pooler, Ga. “With the crop year that just started, prices have remained in the 35 cents per pound to 40 cents per pound range. While 2009 high-fructose corn syrup (HFCS) prices have not yet been announced, expectations are that prices may be raised 3 cents per wet pound to 6 cents per wet pound from current levels. So dairies in particular are going to feel a cost crunch on their sweeteners.

“For several years Sweetener Solutions has been showing dairies how they can save significant sweetener costs by replacing 20% to 35% of their liquid sugar and/or HFCS with our alternative sweetener blend of maltodextrin and neotame,” says Curry. “Replacing 20% of nutritive sweeteners can result in dairy batch savings of close to 15% of overall sweetener costs. This substitution works particularly well in fruit drinks, teas and flavored milks for retail sale. Unfortunately, current school lunch programs prohibit the use of high-intensity sweeteners in flavored milk.”

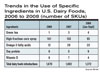

Without a doubt, dairy foods manufacturers are trying to phase HFCS out of products. This is particularly apparent when looking at new product introduction data. According to Mintel International, Chicago, 9.6% of all new dairy foods introduced in 2006 listed HFCS in the ingredient statement. A year later this figure dropped to 8.0%. This year that figure is on track to be even lower. For the first nine months of 2008, only 6.8% of all new dairy foods included HFCS in the formulation.

There’s been an impressive increase in the number of new dairy foods including functional ingredients such as green tea and omega-3 fatty acids. And even though the number of new products fortified with vitamin D is low, this is expected to change very soon as the result of a recently approved health claim linking foods that are excellent sources of both calcium and vitamin D with a reduction in the risk for developing osteoporosis.

According to a new technical market research report from BCC Research, Wellesley, Mass., entitled Nutraceuticals: Global Markets and Processing Technologies, the global market for nutraceuticals was worth $117.3 billion in 2007. This is expected to increase to $123.9 billion in 2008 and reach $176.7 billion in 2013, which is reflective of a compound annual growth rate (CAGR) of 7.4%.

The global nutraceutical market is defined as aggregate sales of functional food, beverage and supplements fortified with bioactive ingredients including fiber, probiotics, protein and peptides, omega-3 fatty acids, phytochemicals, and vitamins and minerals.

The market is broken down into nutraceutical foods, beverages and supplements. Nutraceutical foods were the largest market segment in 2007, worth $39.9 billion. This is expected to increase to $40.6 billion in 2008 and $56.7 billion in 2013. Nutraceutical beverages represent the fastest-growing segment, and are expected to have the largest share of the market by 2013.

The total functional food, beverage and supplement market is known as being a premium business, and thereby makes the market fatter in terms of net sales. The United States is leading the global nutraceutical market with more than 32.8% of the global market share, according to BCC Research.

According to Global Industry Analysts, Inc., San Jose, Calif., the dairy products market is experiencing sturdy growth driven by an onrush of new products intended to meet the demands of both health-conscious consumers and indulgence-seekers. Future market expansion will depend upon unique flavor and ingredient combinations, novel packaging and pack formats, and aggressive marketing.

Manufacturers are expected to continue to deliver stronger and wider product assortments including value-added, functional, convenient, ready-to-eat dairy products targeted to dieters with busy lifestyles. Rising health awareness is expected to provide growth opportunities for participants touting light, low-fat, nonfat or sugar-free claims on their products.

Despite rising costs, dairy foods sales continue to show momentum. This is one aspect of the economy we do not want to change.

First, here’s what it is. Melamine is a simple chemical compound. Resembling a hexagon, melamine is composed of three carbon atoms and three nitrogen atoms. Three arms connect to the hexagon. Each arm has a nitrogen atom and two hydrogen atoms. In other words, melamine is a chemical containing three carbon atoms, six hydrogen atoms and six nitrogen atoms per molecule. By weight the molecule contains 64% nitrogen, which is the reason it is showing up in food.

Historically, melamine is an extremely useful chemical in the plastics business. Mixed with formaldehyde (that in itself sounds scary, too), melamine forms a moldable resin. Everyday plastics containing melamine include formica, dry-erase boards, floor tile and even plates, bowls and cups. But we don’t eat these items. However, when dishes say they are not microwave safe, this is the reason. Melamine heats quickly, and can cause plastic to bubble. You don’t want the melamine leaching into food.

Melamine is also a deadly chemical when consumed. It enters the kidneys, potentially causing failure. During the past year there have been many stories about melamine’s presence in the food supply. It started in 2007 when pet food was found to contain melamine-contaminated wheat gluten. Thousands of animals became sick; many died from kidney failure.

Now we are hearing about contaminated infant formula. Melamine in the formula is poisoning tens of thousands of babies in China, and there is concern that the chemical is making its way into the mainstream food supply in the form of milk or powdered milk that is used as an ingredient in food products made in China.

Are we eating plastic?

Plastic is not being ground up and mixed into foods, nor is it leaching into foods through contact with food. But melamine-the chemical that contains 64% nitrogen-is being added to food in a very deceptive manner, at the expense of lives. See, melamine happens to be very inexpensive and it is produced in abundance in China.

Food contains nitrogen, which comes mostly from protein. Carbohydrates, fats and water, the three other primary constituents of most foods, do not contain any nitrogen. When labs perform compositional analysis of foods, protein content is typically determined by measuring nitrogen levels, which is a relatively simple test. Here’s where the deception takes place.

Imagine you are a food company wanting to improve your bottom line. One way to do this is to sell more water and less protein, as water is essentially free from the tap. Protein comes with a price tag. A product like milk or infant formula can easily be diluted through the addition of water, but, lab tests will show a reduced concentration of nitrogen, and hence protein. An unscrupulous food manufacturer fixes the problem through the addition of-you guessed it-melamine.

Explain this to consumers

It is important for consumers to understand the origins of the melamine in Chinese milk. Also, that this is not a practice that takes place in the States . . . or any other developed country.

If you purchase milk ingredients to fortify dairy foods, make sure you buy domestically produced product. Consumers are reading labels and questioning country of origin for ingredients of concern, such as the nonfat dry milk used in foods from China.

In conclusion, to answer the question posed in the article’s title: No, melamine is not a food ingredient.

Eligible dairy foods include reduced-fat, low-fat and fat-free milk. Yogurts sufficiently fortified in order to be an excellent source-20% or more of the Daily Value-of vitamin D qualify, as do some other dairy products that are excellent sources of both calcium and vitamin D, per standard serving.

Very few foods are inherent sources of vitamin D. In fact, fortified foods provide most of the vitamin D in the American diet. (Sunlight is the non-dietary source of vitamin D, but excessive exposure can be harmful, and thus is not the preferred method for getting your daily dose of this powerhouse nutrient.) Almost all of the U.S. milk supply is fortified with 100 International Units (IU) of vitamin D per 8-oz serving. The Daily Value (DV) for vitamin D has been set as 400 IU, but need increases with age, and also other health variables.

Food labels are not required to list vitamin D content unless a food has been fortified with this nutrient. Foods providing 20% or more of the DV are considered to be excellent sources of this nutrient.

When fortification began

In the 1930s, a vitamin D milk fortification program was implemented in the United States to combat rickets, a deforming bone malformation, among growing children. This program virtually eliminated the disorder at that time; however, data shows that as a result of Americans consuming less milk, rickets has returned as a childhood health concern. The current Code of Federal Regulations states that if milk is fortified with vitamin D, every quart must contain 400 International Units.

Historically, dairy products made from milk, such as cheese, ice cream and yogurt have not been fortified with vitamin D. But this is likely to change with the new approved health claim, as very few foods are recognized as an excellent source of both vitamin D and calcium. In fact, in the United States, only a handful of foods are allowed to be fortified with vitamin D. This includes cereal flours and related products, milk and products made from milk, and calcium-fortified fruit juices and drinks. This is good news for dairy foods and an excellent opportunity to fortify more products and promote inclusion using the new health claim.

There are two types of vitamin D ingredients available for fortification. One is ergocalciferol, or simply vitamin D2. The other is cholecalciferol, which goes by the more common name of vitamin D3. Vitamin D2 is synthesized by plants, while vitamin D3 is synthesized by animals. The latter is also the form humans make in the skin when exposed to the ultraviolet-B rays of sunlight.

For ingredient manufacturing, most vitamin D2 is derived from yeast, while vitamin D3 tends to come from sheep’s lanolin. Though there has been some published research suggesting that vitamin D3 is more potent and bioactive than vitamin D2, food manufacturers are often reluctant to use it, as lanolin presents issues for vegans. This, of course, is not a problem with dairy foods, because vegans avoid dairy anyway.

The dairy industry is poised to make dairy foods the primary dietary source of both calcium and vitamin D through adequate fortification and consumer education.

“Current consumption data indicate that most people aren’t getting enough vitamin D or calcium. The new health claim helps communicate the critical need for calcium, vitamin D and physical activity and their role in reducing the risk of osteoporosis,” says Frank Greer, a medical doctor and chairman of the American Academy of Pediatrics Committee on Nutrition. “Nutrient-rich dairy foods are critical for building strong bones and preventing osteoporosis later in life.”

Here’s more good news to brighten retail sales of vitamin-D fortified dairy foods. The Milk Processor Education Program (MilkPEP) is in the midst of launching the Liquid Sunshine feature incentive program. The retail promotion period runs March 8 to April 4. MilkPEP’s Liquid Sunshine promotion is all about getting your vitamin D via milk and dairy foods, and not the sun’s harmful rays.

Together, we can make dairy foods radiant!

This is quite challenging when prices for most U.S. agricultural commodities and crop-derived ingredients have exhibited extreme volatility in 2008 and are currently at record levels. For example, in May, Cognis Nutrition & Health, La Grange, Ill., announced its first price increase in more than six years for its natural-source vitamin E and natural plant sterol products. “The rapid escalation in raw material costs plus the steady increase in energy, transportation and packaging costs have reached a point that we can no longer maintain current prices,” said Dave Eckert, vice president North America.

The story was the same for many other ingredient suppliers that provide to the dairy industry. In August, BENEO-Orafti, Morris Plains, N.J., said it would increase the price of its natural, chicory-derived prebiotics by 25%. And in October, FMC BioPolymer, Philadelphia, announced a minimum 15% price increase for all products, as contracts allow. The increase affects microcrystalline cellulose, carrageenan, alginates and propylene glycol alginate product lines.

Dominique Speleers, managing director of BENEO-Orafti explained, “BENEO-Orafti has strived to avoid this price increase and has made many improvements within the business to make sure it is running as efficiently as possible. “However, due to the continued and unprecedented increases we have experienced in energy, raw materials and processing costs, a price increase is inevitable and necessary to cover costs and maintain profitability.

“We understand this price increase means extra pressure for our partners and customers. We do know, however, that the consumer recognizes the value and benefits of healthy nutritious foods and is willing and prepared to pay a price premium for such value-added products,” said Speleers.

No time to go back

Speleers is right on target. The dairy industry must stay on track and not produce inferior product. The industry must continue to add value to milk through the innovative application of ingredients. This is not a time to retreat to improve the bottom line; rather dairy marketers must make sure frugal consumers do not cut dairy foods from their shopping list. The message to consumers must be that nutrient-dense powerhouse dairy foods deliver more bang for the buck, especially when all food prices have inflated.Indeed, consumers can change their mode of transportation, and even cut back on entertainment and activities, but when it comes to food . . . they must eat. Sure, there are probably fewer steak “date-night” dinners as the home-cooked casserole returns to the family table. But when it comes to dairy foods, the industry has done so much to improve the image of fluid milk and educate consumers about the healthfulness of all dairy foods that we cannot afford to let high prices impact sales.

Sweet solutions

A number of dairy foods rely on some sort of sweetener to make it palatable to Americans. With many sweeteners, addition is often accompanied by calories. The exception is alternative sweeteners such as lower-calorie sugar alcohols and high-intensity sweeteners. The latter have historically been shunned by parents and schools because of their “artificial” reputation; however, what the industry is learning is that blending all types of sweeteners can save manufacturers money and consumers from excessive calorie intake.“Refined sugar prices have been elevated during 2008 since the Savannah Sugar Refinery explosion in February,” says John Curry, president, Sweetener Solutions LLC, Pooler, Ga. “With the crop year that just started, prices have remained in the 35 cents per pound to 40 cents per pound range. While 2009 high-fructose corn syrup (HFCS) prices have not yet been announced, expectations are that prices may be raised 3 cents per wet pound to 6 cents per wet pound from current levels. So dairies in particular are going to feel a cost crunch on their sweeteners.

“For several years Sweetener Solutions has been showing dairies how they can save significant sweetener costs by replacing 20% to 35% of their liquid sugar and/or HFCS with our alternative sweetener blend of maltodextrin and neotame,” says Curry. “Replacing 20% of nutritive sweeteners can result in dairy batch savings of close to 15% of overall sweetener costs. This substitution works particularly well in fruit drinks, teas and flavored milks for retail sale. Unfortunately, current school lunch programs prohibit the use of high-intensity sweeteners in flavored milk.”

Without a doubt, dairy foods manufacturers are trying to phase HFCS out of products. This is particularly apparent when looking at new product introduction data. According to Mintel International, Chicago, 9.6% of all new dairy foods introduced in 2006 listed HFCS in the ingredient statement. A year later this figure dropped to 8.0%. This year that figure is on track to be even lower. For the first nine months of 2008, only 6.8% of all new dairy foods included HFCS in the formulation.

There’s been an impressive increase in the number of new dairy foods including functional ingredients such as green tea and omega-3 fatty acids. And even though the number of new products fortified with vitamin D is low, this is expected to change very soon as the result of a recently approved health claim linking foods that are excellent sources of both calcium and vitamin D with a reduction in the risk for developing osteoporosis.

Ingredients for functional foods

The nutraceutical ingredients just mentioned, as well as many others, will likely increase in presence in dairy foods, particularly dairy-based beverages, as sales of functional foods continue to grow around the world.According to a new technical market research report from BCC Research, Wellesley, Mass., entitled Nutraceuticals: Global Markets and Processing Technologies, the global market for nutraceuticals was worth $117.3 billion in 2007. This is expected to increase to $123.9 billion in 2008 and reach $176.7 billion in 2013, which is reflective of a compound annual growth rate (CAGR) of 7.4%.

The global nutraceutical market is defined as aggregate sales of functional food, beverage and supplements fortified with bioactive ingredients including fiber, probiotics, protein and peptides, omega-3 fatty acids, phytochemicals, and vitamins and minerals.

The market is broken down into nutraceutical foods, beverages and supplements. Nutraceutical foods were the largest market segment in 2007, worth $39.9 billion. This is expected to increase to $40.6 billion in 2008 and $56.7 billion in 2013. Nutraceutical beverages represent the fastest-growing segment, and are expected to have the largest share of the market by 2013.

The total functional food, beverage and supplement market is known as being a premium business, and thereby makes the market fatter in terms of net sales. The United States is leading the global nutraceutical market with more than 32.8% of the global market share, according to BCC Research.

According to Global Industry Analysts, Inc., San Jose, Calif., the dairy products market is experiencing sturdy growth driven by an onrush of new products intended to meet the demands of both health-conscious consumers and indulgence-seekers. Future market expansion will depend upon unique flavor and ingredient combinations, novel packaging and pack formats, and aggressive marketing.

Manufacturers are expected to continue to deliver stronger and wider product assortments including value-added, functional, convenient, ready-to-eat dairy products targeted to dieters with busy lifestyles. Rising health awareness is expected to provide growth opportunities for participants touting light, low-fat, nonfat or sugar-free claims on their products.

Despite rising costs, dairy foods sales continue to show momentum. This is one aspect of the economy we do not want to change.

Fast facts

- Despite rising ingredient costs, adding value to dairy foods through the addition of functional ingredients is the best approach to ensure healthy category growth both domestically and abroad.

- The United States is the leading global nutraceutical market, with beverages driving growth.

- Sugar is sugar, even when it is labeled as high-fructose corn syrup. However, because perception and reality are often scientifically conflicting, high-fructose corn syrup is being used less often by food formulators.

- The calcium in dairy foods does a better job at preventing the risk of osteoporosis when vitamin D is present. FDA recognizes this, and has approved a health claim suggesting such a synergistic effect. Adding vitamin D to dairy foods other than milk is no longer a “should we?” rather a “how quickly can we?”

- Finally, melamine is not a food ingredient! It should not be in the food supply. Melamine kills.

Is Melamine a Food Ingredient?

It’s impossible to ignore, yet difficult to understand: melamine. What is this chemical and why is it showing up in our food supply?First, here’s what it is. Melamine is a simple chemical compound. Resembling a hexagon, melamine is composed of three carbon atoms and three nitrogen atoms. Three arms connect to the hexagon. Each arm has a nitrogen atom and two hydrogen atoms. In other words, melamine is a chemical containing three carbon atoms, six hydrogen atoms and six nitrogen atoms per molecule. By weight the molecule contains 64% nitrogen, which is the reason it is showing up in food.

Historically, melamine is an extremely useful chemical in the plastics business. Mixed with formaldehyde (that in itself sounds scary, too), melamine forms a moldable resin. Everyday plastics containing melamine include formica, dry-erase boards, floor tile and even plates, bowls and cups. But we don’t eat these items. However, when dishes say they are not microwave safe, this is the reason. Melamine heats quickly, and can cause plastic to bubble. You don’t want the melamine leaching into food.

Melamine is also a deadly chemical when consumed. It enters the kidneys, potentially causing failure. During the past year there have been many stories about melamine’s presence in the food supply. It started in 2007 when pet food was found to contain melamine-contaminated wheat gluten. Thousands of animals became sick; many died from kidney failure.

Now we are hearing about contaminated infant formula. Melamine in the formula is poisoning tens of thousands of babies in China, and there is concern that the chemical is making its way into the mainstream food supply in the form of milk or powdered milk that is used as an ingredient in food products made in China.

Are we eating plastic?

Plastic is not being ground up and mixed into foods, nor is it leaching into foods through contact with food. But melamine-the chemical that contains 64% nitrogen-is being added to food in a very deceptive manner, at the expense of lives. See, melamine happens to be very inexpensive and it is produced in abundance in China.

Food contains nitrogen, which comes mostly from protein. Carbohydrates, fats and water, the three other primary constituents of most foods, do not contain any nitrogen. When labs perform compositional analysis of foods, protein content is typically determined by measuring nitrogen levels, which is a relatively simple test. Here’s where the deception takes place.

Imagine you are a food company wanting to improve your bottom line. One way to do this is to sell more water and less protein, as water is essentially free from the tap. Protein comes with a price tag. A product like milk or infant formula can easily be diluted through the addition of water, but, lab tests will show a reduced concentration of nitrogen, and hence protein. An unscrupulous food manufacturer fixes the problem through the addition of-you guessed it-melamine.

Explain this to consumers

It is important for consumers to understand the origins of the melamine in Chinese milk. Also, that this is not a practice that takes place in the States . . . or any other developed country.

If you purchase milk ingredients to fortify dairy foods, make sure you buy domestically produced product. Consumers are reading labels and questioning country of origin for ingredients of concern, such as the nonfat dry milk used in foods from China.

In conclusion, to answer the question posed in the article’s title: No, melamine is not a food ingredient.

Drinking Up Sunshine

This past month the dairy industry received a long overdue present from FDA: An approved health claim linking calcium and vitamin D with bone health and a reduced risk of osteoporosis. Per the final FDA rule, foods that are an excellent source of both calcium and vitamin D can state the following claim, or other approved language, on package labels: Adequate calcium and vitamin D throughout life, as part of a well-balanced diet, may reduce the risk of osteoporosis.Eligible dairy foods include reduced-fat, low-fat and fat-free milk. Yogurts sufficiently fortified in order to be an excellent source-20% or more of the Daily Value-of vitamin D qualify, as do some other dairy products that are excellent sources of both calcium and vitamin D, per standard serving.

Very few foods are inherent sources of vitamin D. In fact, fortified foods provide most of the vitamin D in the American diet. (Sunlight is the non-dietary source of vitamin D, but excessive exposure can be harmful, and thus is not the preferred method for getting your daily dose of this powerhouse nutrient.) Almost all of the U.S. milk supply is fortified with 100 International Units (IU) of vitamin D per 8-oz serving. The Daily Value (DV) for vitamin D has been set as 400 IU, but need increases with age, and also other health variables.

Food labels are not required to list vitamin D content unless a food has been fortified with this nutrient. Foods providing 20% or more of the DV are considered to be excellent sources of this nutrient.

When fortification began

In the 1930s, a vitamin D milk fortification program was implemented in the United States to combat rickets, a deforming bone malformation, among growing children. This program virtually eliminated the disorder at that time; however, data shows that as a result of Americans consuming less milk, rickets has returned as a childhood health concern. The current Code of Federal Regulations states that if milk is fortified with vitamin D, every quart must contain 400 International Units.

Historically, dairy products made from milk, such as cheese, ice cream and yogurt have not been fortified with vitamin D. But this is likely to change with the new approved health claim, as very few foods are recognized as an excellent source of both vitamin D and calcium. In fact, in the United States, only a handful of foods are allowed to be fortified with vitamin D. This includes cereal flours and related products, milk and products made from milk, and calcium-fortified fruit juices and drinks. This is good news for dairy foods and an excellent opportunity to fortify more products and promote inclusion using the new health claim.

There are two types of vitamin D ingredients available for fortification. One is ergocalciferol, or simply vitamin D2. The other is cholecalciferol, which goes by the more common name of vitamin D3. Vitamin D2 is synthesized by plants, while vitamin D3 is synthesized by animals. The latter is also the form humans make in the skin when exposed to the ultraviolet-B rays of sunlight.

For ingredient manufacturing, most vitamin D2 is derived from yeast, while vitamin D3 tends to come from sheep’s lanolin. Though there has been some published research suggesting that vitamin D3 is more potent and bioactive than vitamin D2, food manufacturers are often reluctant to use it, as lanolin presents issues for vegans. This, of course, is not a problem with dairy foods, because vegans avoid dairy anyway.

The dairy industry is poised to make dairy foods the primary dietary source of both calcium and vitamin D through adequate fortification and consumer education.

“Current consumption data indicate that most people aren’t getting enough vitamin D or calcium. The new health claim helps communicate the critical need for calcium, vitamin D and physical activity and their role in reducing the risk of osteoporosis,” says Frank Greer, a medical doctor and chairman of the American Academy of Pediatrics Committee on Nutrition. “Nutrient-rich dairy foods are critical for building strong bones and preventing osteoporosis later in life.”

Here’s more good news to brighten retail sales of vitamin-D fortified dairy foods. The Milk Processor Education Program (MilkPEP) is in the midst of launching the Liquid Sunshine feature incentive program. The retail promotion period runs March 8 to April 4. MilkPEP’s Liquid Sunshine promotion is all about getting your vitamin D via milk and dairy foods, and not the sun’s harmful rays.

Together, we can make dairy foods radiant!

Links

- State of the Industry 2008: Cheese is Convenient, Naturally

- State of the Industry 2008: Ice Cream--Sweet Success

- State of the Industry 2008: Yogurt Still the Bright Spot

- State of the Industry 2008: Butter--Spreading What's New

- State of the Industry 2008: Changes in the Big Beverage Market

- State of the Industry 2008: Introduction

- State of the Industry 2008: Milk--Ups and Dows

- Chr Hansen

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!