Recent health and wellness trends have impacted – but not hurt – the ice cream and frozen novelties market. U.S. manufacturers are wisely staying abreast of the latest health trends, new products and innovative ingredients to keep their products relevant, yet still enticing.

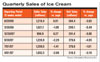

Despite the ice cream and frozen novelties market’s maturity, Mintel reports that it gained roughly 4% per annum from 2002 to 2007. Mintel values the total market at $12.4 billion for 2007, a nearly 20% growth from 2002 when it was valued at $10.4 billion. Because the ice cream and novelty category already has a well-established class of products - giving manufacturers little room to maneuver and few new consumers to attract - this steady growth is a positive sign for the industry.

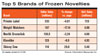

Within the category, traditional packaged ice cream emerges as the clear sales driver, comprising nearly 60% of the total retail market in 2007. Frozen novelties fall into second place with just over a third (36%) of sales, according to Mintel. Sherbet and frozen yogurt combined accounted for just 5% of category sales during 2007.

Screaming for ice cream

Americans’ preference for ice cream over other frozen dessert options is reflected in Mintel’s consumer survey findings. Nearly nine in 10 adults (89%) report eating ice cream, followed by 59% of adults who say they eat frozen novelties. Among children, the preference for ice cream is even stronger: Mintel reports that 98% of children eat ice cream.Fewer than two in five American adults eat sherbet or frozen yogurt, and only 14% say they eat gelato. Mintel views these “ice cream alternatives,” all of which have a healthier profile than traditional full-fat ice cream, as a good place for manufacturers to focus when developing new products.

When it comes to “healthier” ice cream, most new product innovations aim to convince consumers that “low in” treats can actually taste good. Previous lower-fat ice creams were disappointing in both flavor and texture, making consumers hesitant to try them again. But with “churned” technology, manufacturers found a way to provide both full-fat flavor and creamy texture, along with better-for-you positioning.

Packaging for new churned products focuses primarily on taste and texture, almost more than the product’s lower fat and calorie nature. Case in point: Lovin’ Scoopful Churned Light Ice Cream in Out Of This World Chocolate, or Dreyer’s Slow Churned Rich & Creamy Take the Cake Light Ice Cream.

On the fringe

Beyond making traditional ice cream healthier, manufacturers can find ample opportunity in naturally lighter alternatives to ice cream. Gelato, sorbet and frozen yogurt all have healthier profiles, but their consumption in the United States isn’t strong. As healthy eating trends become more commonplace, however, Mintel predicts more Americans will turn to these better-for-you alternatives.Mintel’s consumer survey revealed that fewer than two in five adults (39%) prefer frozen yogurt to ice cream. People do value its health attributes - nearly 90% of Mintel’s respondents think frozen yogurt is healthier than ice cream - but it doesn’t top out on taste and texture. Gelato and sorbet, though, with healthier profiles and premium positioning, represent profitable avenues for frozen dessert manufacturers.

Gelato - the dense, creamy Italian counterpart to American ice cream - appears to be gaining in popularity, both among processors and consumers. Likely the result of increased international travel and a desire for exotic, regional foods, more Americans are reaching for gelato. Mintel’s consumer research shows that nearly eight in 10 adults eat gelato for “something different” occasionally. Furthermore, 45% of consumers like the texture and consistency of gelato over ice cream and 36% think it tastes better.

Gelato is most commonly positioned as an indulgent treat, but sorbet - a dairy-free ice cream alternative - walks the delicate line between decadence and health. Typically made with natural fruit ingredients, sorbet allows consumers to treat themselves to delicious flavor without sacrificing nutrition. The sorbet category has been driven into success primarily by Häagen-Dazs. Positioned as premium, Häagen-Dazs single-handedly generated nearly 86% of segment sales growth from 2005 to 2007. Private label brands, such as Target’s Archer Farms, are now starting to get in on the action.

Other trends

Another way manufacturers are tapping health and wellness trends is by innovating new portion-controlled frozen novelties. A wise extension of the 100-calorie pack trend that first appeared in snacks, portion-controlled ice cream treats meet two consumer desires: controlled calories/fat/sugar and convenience.Mintel’s survey revealed that 43% of Americans would like to see more of their favorite ice cream flavors “on a stick” or in another portable format. Convenience is in and, with the health profile of 100-calorie portions, these new frozen novelty treats are taking the category in exciting new directions.

From bite-sized indulgences to lighter versions of traditional favorites, manufacturers are playing with the portionable concept. Target recently launched Market Pantry 100 Calorie Mini Ice Cream Cones – a shrunken, lower-calorie version of the familiar ready-made cones. Choco’s Ice Cream Bon Bons likewise offer portionability, but without the obvious “diet” positioning. Described as rich premium ice cream cookies covered in chocolate, each luscious morsel contains 60 calories, 4 grams of fat and 6 grams of carbohydrates. They are diet-friendly and convenient, even without trying to be.

Organic ice creams in particular have gained traction in grocery freezers. According to Mintel GNPD, U.S. organic ice cream and frozen novelty launches more than doubled from 2005 to 2007. Already in 2008, manufacturers have launched 56 new organic products, suggesting a continued upswing for the segment.

The rise of organic ice creams has also paved the way for the category’s newest sustainability trend: fair trade. Ben & Jerry’s was the first player in the fair-trade ice cream space, featuring Fair Trade Certified coffee in its coffee-flavored ice creams as early as 2005. Other brands, such as Luna & Larry’s and Stonyfield Farm, have recently caught on and begun featuring fair-trade ingredients in their frozen desserts. Mintel expects growth here as manufacturers find ways to make their products more environmentally and human-friendly.

A sweet future

Despite challenges posed by rising commodity prices, economic woes and health concerns, Mintel expects steady sales increases for the ice cream and frozen novelties market. From 2008 to 2012, Mintel forecasts that the market will grow 15%. Much of this growth is expected to come from innovations in frozen novelties and healthy positioning in this formerly “unhealthy” category. Manufacturers who can find the delicate balance between health and indulgence are poised to have the sweetest success.Fast Facts

- 589 new ice cream and frozen dessert products were launched between January and September of this year. That’s just 10 more than were introduced in 2003 but about half as many as in 2006.

- Kosher led product claims of U.S. ice cream and frozen dessert products launched between September 2007 and September 2008, followed by no/low/reduced fat and premium.

- 56 organic products were launched during the same period.

- Since hitting the scene five years ago, “churned” products hit a peak in 2006 with 112 launches.

- Total sales of ice cream and frozen desserts are expected to rise $1.8 billion by 2012.

Links

- State of the Industry 2008: Cheese is Convenient, Naturally

- State of the Industry 2008: Yogurt Still the Bright Spot

- State of the Industry 2008: Butter--Spreading What's New

- State of the Industry 2008: Changes in the Big Beverage Market

- State of the Industry 2008: Ingredients--Pricey Necessities

- State of the Industry 2008: Introduction

- State of the Industry 2008: Milk--Ups and Dows

- National Starch